Court felt that it “…is difficult to see how a seizure contemplated by the Impugned Provisions significantly intrudes into privacy interests, as the appellants appear to suggest”. See the decision.

This announcement includes a link to the decision.

Court felt that it “…is difficult to see how a seizure contemplated by the Impugned Provisions significantly intrudes into privacy interests, as the appellants appear to suggest”. See the decision.

This announcement includes a link to the decision.

CANADIAN FATCA LITIGATION UPDATE December 7, 2019:

You are contributing to raising the money needed to pay the legal costs to litigate with the Government of Canada — to prevent Canada from imposing the U.S. FATCA law directly on Canada and Canadians.

The Alliance for the Defence of Canadian Sovereignty and Gwen and Kazia have raised $24,612 in this funding round. We ask you for $20,388 in EIGHT DAYS to make $45,000 December 15 payment for appeal of FATCA Federal Court decisions.

You can DONATE by cheque, cash, PayPal (easiest) and transfers.

Gwen and Kazia, two brave Canadian citizens having no meaningful relationship with the U.S., are appealing on your behalf two Federal Court decisions to the Canadian Court of Appeal.

The grounds for appeal will include violations against their autonomy (Charter section 7), privacy (8) and equality (15) as well as arguments that the ruling was improperly based on the finding that the Income Tax Act is primarily regulatory in nature, and that factors such as the relationship between Canada and United States were not properly dealt with. Fleshed out details of appeal grounds will be provided in the Factum, likely early next year.

Gwen and Kazia ask for your help in paying for the legal costs of the appeal. If you feel that FATCA IGA laws harm you or someone that you know, PLEASE DONATE.

CANADIAN FATCA LITIGATION UPDATE September 30, 2019: Gwen and Kazia file Notice of Appeal

Appellants Gwen and Kazia have instructed Vancouver lawyer Mr. Greg Delbigio to appeal the Martineau and Mactavish Canadian Federal Court FATCA IGA legislation decisions.

A brief Notice of Appeal was just filed today (September 30, 2019) with the Canadian Federal Court of Appeal. The grounds for appeal will evolve and be broadened with detail at later stages. For the appeal process to continue we will need to raise monies quickly to pay for the legal costs.

The US Government Accountability Office has released an 83 page Report to Congressional Committees, “Foreign Asset Reporting: Actions Needed to Enhance Compliance Efforts, Eliminate Overlapping Requirements, and Mitigate Burdens on U.S. Persons Abroad”. Thanks to JC for posting this link on the Media page.

Related Brock post: April 2019 Report From GAO is evidence of how #FATCA and Foreign Asset Reporting is viewed in the Homeland by USCitizenAbroad.

Hot off the press from GAO – important because it illustrates how this issue is viewed in the Homeland: "Foreign Asset Reporting: Actions Needed to Enhance Compliance Efforts, Eliminate Overlapping Requirements, and Mitigate Burdens on U.S. Persons Abroad" https://t.co/T0k4HKll0j

— U.S. Citizen Abroad (@USCitizenAbroad) April 1, 2019

Question:

The above tweet links to the a report from the Government Accountability office. It is extensive but generally interesting. A quick perusal reveals no evidence that the Government views FATCA and foreign asset reporting as tools to enforce worldwide taxation on people who live outside the United States. Yet, that is the purpose of FATCA and foreign asset reporting in general.

The “Fast Facts” page includes:

How does the government prevent tax dodgers from hiding income in offshore accounts?

A 2010 law requires Americans and foreign banks to report more information to IRS about Americans’ foreign assets. Implementing the law, however, has raised some concerns.

For example, close to 75% of taxpayers reporting foreign assets to IRS also reported them separately to Treasury—indicating potential unnecessary duplication.

Also, some Americans living abroad can’t get services from foreign banks that find the law too burdensome.

Our recommendations to Congress, Treasury, and other agencies address challenges related to foreign asset reporting.

The 2010 Foreign Account Tax Compliance Act, known as FATCA, created new reporting requirements for taxpayers with specified foreign asset

Reposted from the Renounce US Citizenship blog

This post was written in December 2014. It is being reposted in 2018 – the question is why

FATCA and the CRS (“Common Reporting Standard”) are mandatory information sharing schemes. They first define people in terms of their “tax residency” (each country defines who its tax residents are) and then shares people’s private information based on that “tax residency”. In other words (assuming you believe that there is a legitimate interest in privacy) both FATCA and the CRS should be viewed as “privacy overrides”.

Although the notion of privacy is dead in the United States (companies like Facebook and Google make a living off obtaining and using private information), the European GDPR suggests that privacy is valued by Europeans and that individuals should have some control over their data. In Europe the GDPR reflects a presumption that individual belongs to the individual. There is no such presumption in the United States. See:

31-year-old Austrian lawyer Max Schrems was the catalyst for new privacy protection regulations in Europe. He says your data belongs to you and you should have control over it. pic.twitter.com/OTV0reXDOg

— 60 Minutes (@60Minutes) November 12, 2018

Automatic exchange of tax information and data privacy

#FATCA Repeal Update: The action to take right now!https://t.co/5xuVgYEvZY

— U.S. Expat Canada (@USExpatCanada) July 27, 2018

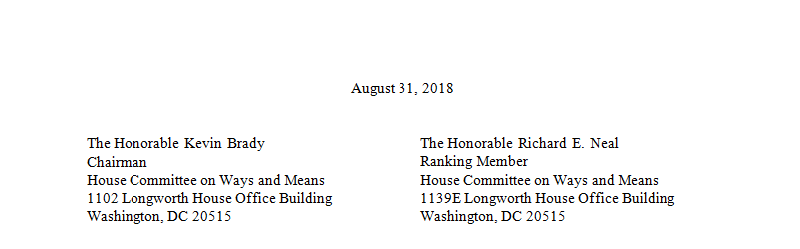

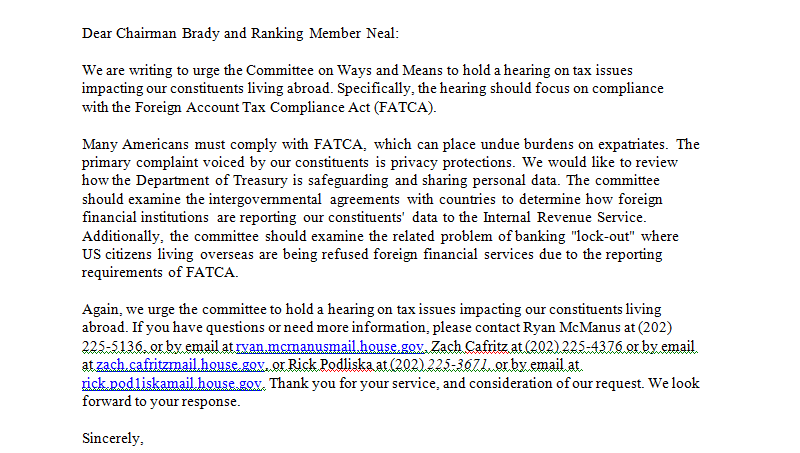

From Global Advocate for the American Overseas, Keith Redmond is this important message:

ATTENTION AMERICANS OVERSEAS!

There is a SERIOUS bi-partisan push for an updated FATCA hearing to address the sharing of personal financial data and the lock-out of Americans overseas from foreign financial institutions (i.e. their local banks).

As a result of Suzanne Iclef Herman’s hard work and tenacity in establishing and cultivating a relationship with her Congressman and his staff, we have succeeded in building bi-partisan momentum in an updated FATCA hearing. Suzanne requested to Congressman Posey’s office that I get involved in order to have as many Americans overseas as possible contact their respective Congressmen/Congresswomen.

The attached letter has been sent to Members of Congress (MOC) in a bi-partisan effort to have the House Ways & Means Committee hold another FATCA hearing. In conjunction with the request, MOCs have been sent a letter (in the same aforementioned attachment) which each MOC can send to House Ways & Means Committee showing their support for another hearing. Americans overseas are asked to write their Congressmen/Congresswomen to sign the letter.

Therefore, I am requesting that you contact your Congressman/Congresswoman via e-mail and/or fax AND FOLLOW-UP WITH A TELEPHONE CALL.

I have attached the THREE STEPS to be taken in order to contact your representative via e-mail as well as the link to find your representative’s fax number. Please follow the instructions.

reprinted with permission from Tax Connections

Prior to the enactment of FATCA, Congress and the Executive were in possession of concrete-evidence revealing FATCA would fail to collect any meaningful amount of tax-revenue from U.S. persons evading tax through offshore financial center holdings. Congress should have halted enactment of HIRE – if in fact, FATCA’s purpose was to collect tax-revenue from offshore tax evasion by U.S. persons.

The United States Congress used estimates from the Joint Committee on Taxation (JCT) as the foundation for supporting the Foreign Account Tax Compliance Act (FATCA), contained in the Hiring Incentives to Restore Employment Act (HIRE).

HIRE was a tax expenditure designed to encourage U.S. small business to hire new employees. HIRE included two tax expenditures of note: a payroll tax exemption to employers and a one-thousand dollar tax credit for employers hiring employees between February of 2010 and January of 2011. [1] FATCA was included in HIRE because the tax revenue collected from FATCA was supposed to offset the tax expenditures authorized by HIRE. [2] The tax revenue FATCA was said to be targeting was from U.S. persons with foreign bank accounts who were evading tax.

In July of 2008, and around the time of the UBS scandal and the Global Financial Crisis the U.S. Senate Permanent Subcommittee on Investigations held a hearing and issued a report entitled “Tax Haven Banks and U.S. Tax Compliance”. [3] The underlying justification for FATCA as a substantial revenue raiser rested on a single statement found in a footnote in the 2008 hearing report: “Each year, the United States loses an estimated $100B in tax revenue due to offshore tax abuses.” [4] In a 2009 follow-up report, the Ways and Means’ Subcommittee on Select Revenue Measures held a hearing entitled: Banking Secrecy Practices and Wealthy Americans. During this hearing, the Senate increased the U.S. tax revenue loss-estimate by 50 percent stating: “Contributing to the annual tax gap are offshore tax schemes responsible for lost tax revenues totaling an estimated $150B each year.” [5] The estimates entered into the record during these hearings measured the offshore tax gap, or the amount of tax revenue[6] that would be collected if offshore tax evasion by U.S. persons holding foreign bank accounts was ended. One month, before HIRE was signed into law by President Obama, new evidence revealed the offshore tax gap was nowhere near as large as previously thought.

On February 23, 2010, the JCT released a report estimating that FATCA would instead, only collect $8.7B over ten-years or $870M per year; a huge difference from last-year’s estimate of $150B per year.[7] Assuming this latest estimate was accurate, the 2008 and 2009 estimates were drastically overinflated – to the tune of over $149B annually! At that point, a reasonable person puts on the breaks and asks questions. At the very least Congress should have engaged in some due diligence to determine why there was such a huge discrepancy. After all, there was plenty of time remaining on the legislative clock,[8] and the report invalidated the policy justification for FATCA. Instead, Congress and President Obama steamrolled FATCA into law in less-than a month after the JCT estimate – almost like, they wanted to hurry to get it in, before someone caught wind that the FATCA had nothing to do with closing the fictitious $150B offshore tax gap, because there was really no tax revenue outstanding. (Part I….To Be Continued)

Continue reading

According to an article by Michael Cohn in Accounting Today, a multi-lateral tax enforcement group has been formed. The Joint Chiefs of Global Tax Enforcement (or J5 for short), intend to “collaborate in fighting international and transnational tax crimes and money laundering.”

U.S., U.K., Canada, Australia and Netherlands form international tax enforcement group https://t.co/x3bX03Ardw Enough Already! We've got Treaties, #FATCA , #CRS When will it end? pic.twitter.com/4DRrjKSVhg

— Citizenship Taxation (@CitizenshipTax) July 1, 2018

Membership of the J5 includes the heads of tax crime and senior officials from Internal Revenue Service Criminal Investigation (IRS CI), Her Majesty’s Revenue & Customs (HMRC) in the U.K., the Australian Criminal Intelligence Commission (ACIC) and Australian Taxation Office (ATO), the Canada Revenue Agency (CRA), and the Dutch Fiscal Information and Investigation Service (FIOD).

Leaders of the group met Thursday in Montreal to formulate their plans. The J5 plans to work together to gather and share information and intelligence, as well as conduct operations and build capacity for tax crime enforcement officials. Areas of focus include cybercrime and cryptocurrency, data analytics, and enablers and facilitators of tax crimes. The alliance will concentrate on building international enforcement capacity, as well as enhancing operational capability by piloting new approaches and conducting joint operations, to bring perpetrators who enable and facilitate offshore tax crime to justice