cross posted from Be careful what you “fix for”! A Holiday Gift: What to do about the unfiled #FBAR

UPDATED WEDNESDAY JANUARY 4, 2017

Part 6 – Getting help with “fixing your compliance problem”:

“The smaller the step taken, the bigger the result”

Some tax professionals:

– believe that compliance problems should presumptively be solved ONLY through prescribed IRS procedures including: “Streamlined (domestic or offshore)”,”OVDP”

“Delinquent information returns” and; “Delinquent FBAR submission procedures”; AND THEREFORE

– rightly or wrongly (and it depends on the facts) find it difficult to deal with the Title 31 FBAR problem without considering one or more Title 26 tax problems.

In many cases they will frame the issue as:

Should you use OVDP (the answer is almost always NO) or should you use Streamlined (the answer is usually maybe). But, to use either OVDP or Streamlined is to NOT solve the Title 31 FBAR problem without compounding the number of problems (by introducing Title 26 tax issues). Are you eligible to use the “Delinquent FBAR submission procedures?”

The threshold consideration is whether all income associated with the “foreign accounts”, that should have been reported on the tax returns was properly reported.

OVDP and Streamlined ALWAYS assume more than one problem …

Since OVDP and Streamlined deny the possibility of solving the Title 31 FBAR problem on its own, some advisers escalate one simple Title 31 FBAR problem into several problems.

OVDP, Streamlined the “Delinquent FBAR Filing Procedures” are NOT not found in either the Internal Revenue Code (Title 26) or the Bank Secrecy At (Title 31). Therefore, they are NOT the law and are NOT legally required. They may or may not be advisable courses of action.

(This is where your adviser can assist you in making a rational decision.)

Obeying the law (“doing the right thing”) requires two things.

Thou shalt:

1. File FBARs (Title 31)

2. File your tax returns (Title 26)

What could be wrong with fixing “compliance problems” by “obeying the law”?

Isn’t to “obey the law”, to “do the right thing”?

There are people who fix their “compliance problems” by simply “filing their tax returns and/or amended tax returns” without using OVDP or Streamlined. In do doing, they are simply “obeying the law”. You will find many “internet warnings” against filing tax returns outside of the OVDP or Streamlined (“quiet disclosures“). Are these warnings justified?

Is it really “the wrong thing” to try to “do the right thing”

(obey the law)?

The answer depends on the facts. I will address the question of “quiet disclosures” in a separate post.

“The total weight of problems is equal to the square of the number of problems!”

You will compound your problems by allowing your problems to escalate.

That’s how the two people described above, who started with one simple problem, found themselves in the messes they are in today.

Conclusion: consider whether you can deal with minor/unintentional FBAR violations as a “stand alone single problem”.

There may be no need to escalate that one single problem into a multi-dimensional full blown tax problem!

Remember: In most cases, “the smaller the step taken, the bigger the result for you!”

*******

Part 5 – Focusing specifically on the problem of FBAR non-compliance

In the beginning, your goal is to “obey the law” (which is a great idea) …

At the risk of oversimplification, as a U.S. citizen resident (Green Card Holder, U.S. citizen, or someone who meets the substantial presence test) you must comply with the rules of at least two separate U.S. statutes:

Title 31 – AKA “The law of Mr. FBAR”

Title 26 – AKA “The law of taxes”

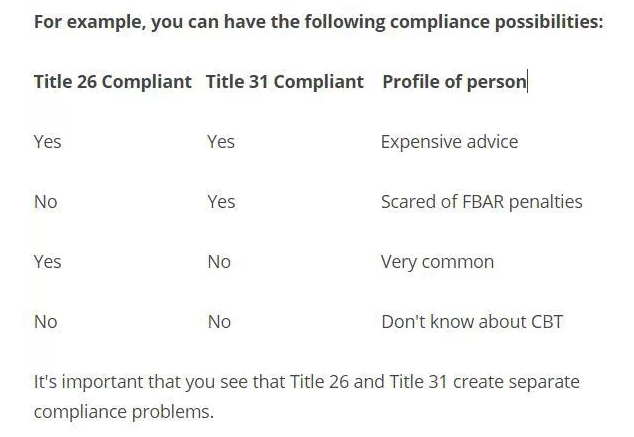

It’s important to understand that Title 31 and Title 26 are separate statutes with separate issues. They are logically unrelated.

One can have the following compliance possibilities:

Let’s stay focussed on the Title 31 (Mr. FBAR) problem …

The first step is to see if the Title 31 FBAR problem can be solved independently of dealing with the Title 26 (tax issues). Let’s consider both what the law of FBAR says and what the IRS says.

The law: Even Mr. FBAR is subject to the law …

The FBAR reporting provision is found in S. 5314 of Title 31.

The “criminal penalty” provisions are found in S. 5322 of Title 31.

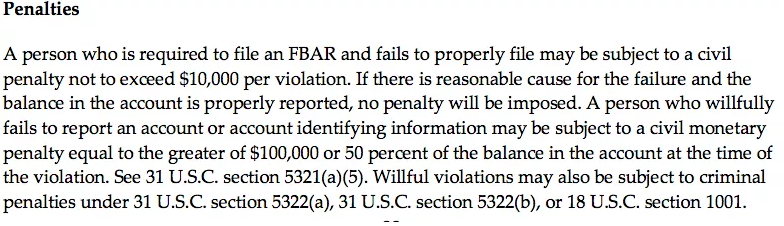

The “civil penalty” provisions are found in S. 5321 of Title 31:

(5) Foreign financial agency transaction violation.—

(A)Penalty authorized.—

The Secretary of the Treasury may impose* a civil money penalty on any person who violates, or causes any violation of, any provision of section 5314.(B) Amount of penalty.—

(i)In general.—

Except as provided in subparagraph (C), the amount of any civil penalty imposed under subparagraph (A) shall not exceed $10,000.

(ii)Reasonable cause exception.— No penalty shall be imposed** under subparagraph (A) with respect to any violation if—

(I) such violation was due to reasonable cause***, and

(II) the amount of the transaction or the balance in the account at the time of the transaction was properly reported****.(C)Willful violations.—In the case of any person willfully violating*****, or willfully causing any violation of, any provision of section 5314—

(i) the maximum penalty under subparagraph (B)(i) shall be increased to the greater of—

(I) $100,000, or

(II) 50 percent of the amount determined under subparagraph (D), and

(ii) subparagraph (B)(ii) shall not apply.(D)Amount.—The amount determined under this subparagraph is—

(i) in the case of a violation involving a transaction, the amount of the transaction, or

(ii) in the case of a violation involving a failure to report the existence of an account or any identifying information required to be provided with respect to an account, the balance in the account at the time of the violation******.

*”may impose” – note that there is NO mandatory penalty. In fact, if you read the IRS penalty mitigation guidelines, you will see that in many cases a “warning letter” will suffice.

**”no penalty shall be imposed” – in certain circumstances (at least in

theory) the IRS is statutorily barred from imposing a penalty

***”due to reasonable cause” – impossible to know with certainty what reasonable cause means. But, there have been few FBAR penalties imposed on “innocent offenders”. Ask: “Was it reasonable in your circumstances for you to have not known about the FBAR rules? See this interesting account of “reasonable cause arguments” in the context of OVDI.

****”was properly reported” – hard to know exactly what this means. But, it suggests that if you report the account by filing an FBAR that the account “was properly reported”.

*****”willfully violating” – recent Court decisions (example McBride, Williams and Bohanec make it clear that in the “civil penalty context”, “willfulness can be established based on a “preponderance of the evidence standard .(Remember that this post is written for innocent victims of the FBAR rules who just want to “make it right” by filing an

FBAR.)

******”at the time of the violation” – The penalties are based on the account balance on the day that the FBAR report was due. What if there is no balance in the account on the day that Mr. FBAR is due? On this point, see this interesting analysis, which incorporates this point.

Conclusion with respect to the FBAR statute:

Penalties for FBAR violations are not automatic and please note that they are usually limited in amount. The IRS itself has prepared mitigation guidelines for its agents in applying FBAR penalties. For an expanded discussion of this principle, see the article referenced in the following tweet and see the IRM Mitigation guidelines here.

FBAR Penalty Mitigation Guidelines: Four Easy Steps For Knocking The FBAR Calculation Out of the Park – Deblis Law https://t.co/kJ2yc30All

— Citizenship Lawyer (@ExpatriationLaw) December 23, 2016

Note that the statute itself does NOT condition FBAR penalty relief on the reporting of income (on your 1040) associated with the undisclosed account.

The IRS published guidelines for failure to file Mr. FBAR …

Delinquent FBAR Submission Procedures https://t.co/qjULt0aF7r – how to file Mr. #FBAR outside OVDP or Streamlined compliance

— Citizenship Lawyer (@ExpatriationLaw) December 23, 2016

Since 2014 the IRS has had clear guidelines for how to deal with minor FBAR problems. In many cases it is possible (and always advisable) to deal with FBAR (Title 31) violations without considering any income tax (Title 26) questions. The above tweet links to the IRS guidelines that

include:

Delinquent FBAR Submission Procedures

Taxpayers who do not need to use either the OVDP or the Streamlined Filing Compliance Procedures to file delinquent or amended tax returns to report and pay additional tax, but who:

have not filed a required Report of Foreign Bank and Financial Accounts

(FBAR) (FinCEN Form 114, previously Form TD F 90-22.1),are not under a civil examination or a criminal investigation by the IRS, and have not already been contacted by the IRS about the delinquent FBARs should file the delinquent FBARs according to the FBAR instructions.

Follow these steps to resolve delinquent FBARS

Review the instructions

Include a statement explaining why you are filing the FBARs late

File all FBARs electronically at FinCEN

On the cover page of the electronic form, select a reason for filing late

If you are unable to file electronically, contact FinCEN’s Regulatory Help line at 1-800-949-2732 or 1-703-905-3975 (if calling from outside the United States) to determine possible alternatives to electronic filing.

The IRS will not impose a penalty for the failure to file the delinquent FBARs if you properly reported on your U.S. tax returns, and paid all tax on, the income from the foreign financial accounts reported on the delinquent FBARs, and you have not previously been contacted regarding an income tax examination or a request for delinquent returns for the years for which the delinquent FBARs are submitted.

FBARs will not be automatically subject to audit but may be selected for audit through the existing audit selection processes that are in place for any tax or information returns.

The above statement from the IRS reflects what I would call a “safe harbour provision” for filing FBARS. It applies to those who have reported the “income from the foreign financial account” The IRS (who is responsible for administering the FBAR statute) says:

If you can meet the conditions described above, just file your FBARs and go on your “Merry Way”.

Note again: that the above procedure is available only to those who have “reported the income” income associated with the unreported account.

General conclusion: It may be possible to resolve ALL Title 31 FBAR problems without considering any Title 26 tax problems.

"All You Need To Do Is File Your Delinquent FBARs" via @forbes https://t.co/mwbRScrcmT – For "common sense minded" people

— Citizenship Lawyer (@ExpatriationLaw) December 23, 2016

The above tweet links to an excellent article (with interesting

comments) which reinforces the point that:

“Simple FBAR violations can be resolved in simple ways.”

One problem, one solution.

How simple FBAR problems become expensive and complicated …

The simple answer is that single/simple FBAR problems become multifaceted compliance problems when the issue of “tax compliance” is added to the mix. The reason is simple. If one files amended tax returns then one has an obligation to file those returns correctly (which may mean dealing with multiple tax compliance issues).

Remember:

The total weight of the problems is equal to the square root of the number of problems!

One Title 31 FBAR problem = the weight of one problem.

One Title 31 FBAR problem plus one Title 26 tax problem = the weight of four problems.

*******

Part 4 – How the compliance problems of “Homeland Americans”

(particularly Green Card holders) differ from the compliance problems of “Americans Abroad”

“We are well aware that there are many U.S.citizens who have resided abroad for many years, perhaps even the vast majority of their lives,” Koskinen told a luncheon audience at the 2014 OECD International Tax Conference in Washington. “We have been considering whether these individuals should have an opportunity to come into compliance that doesn’t involve the type of penalties that are appropriate for U.S.-resident taxpayers who were willfully hiding their investments overseas.”

June 2014 Remarks of IRS Commissioner Koskinen as reported by Tax Analysts

The basic difference is that MOST Americans abroad have NOT been filing U.S. taxes and have little or no U.S. tax compliance history. Therefore, not only have they not been filing FBARs, but they have not been filing anything. They have no mistakes in their filings. U.S. residents HAVE generally been filing U.S. taxes. They may NOT have been filings FBARs and other international information returns. They do have mistakes in their filings.

It is generally easier to deal with “total non-compliance” (have filed no tax returns) than to deal with “partial non-compliance” (have filed tax returns with mistakes).

Although the IRS

“Streamlined Program” is available to both Americans abroad and to Homeland Americans, the

“Streamlined offshore program” for Americans abroad, is easier to use than the

“Streamlined domestic program” for Homeland Americans.

(The very fact of filing U.S. tax returns means that U.S. residents are far more likely to encounter Schedule B and it’s questions that ask directly about “foreign bank accounts”). In addition, there is an assumption (almost certainly true) that U.S. residents have better access to U.S. tax help than do Americans abroad. As a result, as noted by numerous commentators, the “statement of non-willfullness for Streamlined” will require more care and detail for “Homeland Americans” than for Americans abroad. In addition, the Streamlined version for Homeland Americans comes with a 5% penalty and the Streamlined version for Americans abroad is “penalty free”.)

Therefore, it is usually easier for “Americans abroad” to “fix” their compliance problems than it is for “Homeland Americans” to “fix” their compliance problems.

We know that “Americans abroad” are composed of definable groups

(“accidental Americans“,

“long term expats“,

“Homelanders abroad“, etc. What do we mean by “Homeland Americans”?

“Homeland Americans are composed of U.S. citizens and Green Card Holders …

It is important to recognize the special problems experienced by Green Card holders.

Koskinen also pointed to taxpayers residing in the United States with offshore accounts “whose prior noncompliance clearly did not constitute willful tax evasion but who, to date, have not had a clear way of coming into compliance that doesn’t involve the threat of substantial penalties.”

“We believe that re-striking this balance between enforcement and voluntary compliance is particularly important at this point in time, given that we are nearing July 1, the effective date of FATCA,” Koskinen said.

June 2014 Remarks of IRS Commissioner Koskinen as reported by Tax Analysts

The perils of overseas tax disclosure: An immigrant's story https://t.co/EtxM9RY6LH via @Reuters – More like "The perils of the #GreenCard"

— Citizenship Lawyer (@ExpatriationLaw) December 24, 2016

The plight of Americans abroad has received some attention. The plight of “Green Card Holders” has received insufficient attention.

The simple reality is that many “Green Card Holders” came to America and

retained bank accounts in their home countries. In the same way that “foreign accounts” are local to Americans abroad, the “foreign accounts” of many Green Card Holders are NOT foreign to them.

The treatment of Green Card Holders in the 2011 OVDI reign of terror was brutal and unconscionable. Many

Green Card Holders entered OVDI and paid penalties for not filing FBARs reporting bank accounts they left behind when they immigrated to the United States. Interesting accounts of Green Card Holders in the 2011 OVDI program are detailed here and

here. In any event, it is shocking that Green Card holders, who attempted to report their foreign bank accounts (obey the

law) upon learning of the FBAR rules, would have been subjected to such brutality by the U.S. government. Once again we see examples of “the harder people try to comply” the “greater the punishment”.

In addition, Green Card holders run the risk of deportation for FBAR and tax related offenses. This issue was canvassed by Virginia La Torre Jeker here. Her post includes:

This recent case raises the stakes for Green Card holders and other US resident aliens who have undisclosed foreign assets or financial accounts. Based upon the

Kawashima holding, a Green Card holder or other resident alien who has elected to make a ”quiet” disclosure, a ”noisy”

(voluntary) disclosure, or who has not yet decided how he will proceed with disclosure of unreported foreign income or assets , can be subject to deportation in the event of a criminal conviction involving these tax matters. While making a “noisy” disclosure through the IRS offshore voluntary disclosure initiative generally removes the chance of any criminal proceedings being brought against the taxpayer, it is not necessarily a foregone conclusion. To date, I do not know of any case when the IRS recommended criminal prosecution for a taxpayer who entered the offshore voluntary disclosure program.If a long-term Green Card holder is deported (or otherwise relinquishes the Green Card), he or she may also be subject to the so called “expatriation” tax provisions, which are the subject of another blog posting. Under these rules, the individual will generally be treated as if he sold all of his worldwide assets at fair market value at such time and will be subject to income tax on the deemed gain.

Additionally, very harsh tax results are imposed on any US person who later receives a gift or bequest from such an expatriate.

(For information on the “Expatriation Tax” AKA “Exit Tax” imposed by Internal Revenue Code S. 877 see here and

here.) In the

words of one former Green Card Holder who

(apparently) naturalized as a U.S. citizen partly because of the “Exit

Tax”:

Remember long term green card holders get all this crap without ever being citizens or even having a right to enter the US. They can be thrown out at the whim of the government and could be large piggy banks that just need a little smash from Obama. The exit tax would be triggered by you been thrown out of the country. This is how I viewed my status. Couples with unlimited marritable exemption being denied for non-citizens you have to become a citizen.

Note that the people who put together the exit tax wanted everybody to be a covered expatriate. How do we know this? The $2M limit in one of the tests legs is not indexed for inflation. I don’t ever believe this is a mistake. For example Obama’s $200k/$250k are not indexed. Everyone should pay higher taxes eventually because that’s what they want.

Compare the $2M to the tax burden leg that is indexed. A average tax burden of $135k is a lot of income over the last three years.

American citizens cannot be deported. Although Americans abroad now have “support groups”, it is NOT evident that similar support groups exist for Green Card holders.

Interestingly, I have recently spoken that a surprisingly large number of Green Card holders who do NOT want to become U.S. citizens.

Part 5 tomorrow!

*******

Part 3 – It often begins with a chance meeting with Mr.

FBAR

During the last few weeks I have had two conversations with U.S.

residents who: (1) believed that they were compliant with their U.S. tax obligations, (2) had non-U.S. bank accounts (for entirely legitimate reasons), (3) didn’t know about the FBAR rules, and (4) in attempting to solve a simple FBAR problem ended up paying legal fees that were astounding (in one case exceeding six figures by a large margin and in the other case approximately $50,000). Needless to say, that is NOT what the clients “thought they were signing up for”. In neither case is the problem resolved. Notice also that they these are people who recognized that they were NOT in compliance with the FBAR rules (which few people know about and fewer understand) and wanted to be in compliance with the FBAR rules. The purpose of this post to explore how this tragedy happened and how it might be avoided.

What happens when you are introduced to Mr. FBAR …

Americans are extremely law abiding people. They commonly live under the assumption that compliance with the law is “the right thing”. Their instincts are generally toward compliance. Therefore, when they learn about Mr. FBAR (perhaps they received a FATCA letter) and the potential for the damage that he can inflict (FBAR is a form of “civil forfeiture), their immediate reaction is:

- Oh My God! – I’m not in compliance

- I want to fix this and file my FBAR.

- FBAR is a law, I am in violation of the law. Please, I just

want to file my FBAR. - I have read all I can on the internet (most of which is

scaremongering) and I still don’t really understand this. - In order to comply with the law I will

call a lawyer or accountant.

A principle to guide you: “The smaller the compliance step taken, the bigger and better the result!”

It’s at this point, that you might discover that what you thought was one problem (Title 31), is potentially two problems (Title 26) (or maybe even more). You must do your best to “contain the problem”. Make every effort to avoid the escalation of problems. Seek advisers who actively seek to prevent the “escalation” of problems.

The governing principle should be:

“The smaller the compliance step taken, the bigger and better the result!”

Why a Title 31 FBAR problem may (or may not) mean a Title 26 tax problem …

It’s because the “foreign bank account” might be generating interest income that may not have been reported on your 1040. Of course a “foreign bank account” may have generated “interest income” that WAS reported on your 1040. Or maybe, that “foreign bank account” might have generated NO income whatsoever (in which case there was nothing to report on the 1040).

*******

Part 2 – Looking For Mr. FBAR

A bit of background – “Looking for Mr. FBAR” …

This post assumes that you understand FBAR basics. For those who wish a “reintroduction” to Mr. FBAR, I recommend the following articles referenced in the following tweets:

Looking for Mr. FBAR – In Search of FBAR Fullfilment and Consciousness https://t.co/obD7PLprhu – AKA #FBAR 101

— Citizenship Lawyer (@ExpatriationLaw) December 23, 2016

Looking for Mr. FBAR? Fast & Digestible FBAR Facts https://t.co/zorTZqjxtN

— Citizenship Lawyer (@ExpatriationLaw) December 23, 2016

Will a business trip to the United States of America trigger a "chance" encounter with Mr. #FB… https://t.co/ajjNIlJIUg via @ExpatriationLaw

— Citizenship Lawyer (@ExpatriationLaw) December 23, 2016

This post is not for the purpose of detailing the FBAR rules. What you

need to know is that:

If a “U.S. Person” (which includes citizens and Green Card holders

regardless of where they actually live):

– has financial accounts (which includes more than bank accounts) which

in aggregate had balances exceeding $10,000.00 USD at any time in the

year;

– information on those accounts must be reported to the Financial Crimes

division of U.S. Treasury

Finding Mr. FBAR: The FBAR rules are the sum of the following

individual components:

A summary of the IRS interpretation of the FBAR rules and regulations

may be found here. In summary, the FBAR rules are found in three

distinct places:

- Congressional legislation – Title 31 Bank Secrecy

Act – Generally:

https://www.law.cornell.edu/uscode/text/31/subtitle-IV/chapter-53/subchapter-II

and Primarily: General reporting requirement

https://www.law.cornell.edu/uscode/text/31/5314),

Civll penalty

https://www.law.cornell.edu/uscode/text/31/5321

and Criminal penalty

https://www.law.cornell.edu/uscode/text/31/5322 - Regulations made pursuant to the Congressional

legislation -Primarily:

https://www.law.cornell.edu/cfr/text/31/1010.350 - The

FBAR form and

instructions.

Clearly, almost all Americans abroad would be impacted by this rule.

The failure to report these accounts can lead to confiscatory penalties and even (in some cases) criminal charges. FBAR violations can generate both “civil” and “criminal” penalties. See for example the cases of

Marie Curran,

Carl Zwerener,

Dan Horsky and others.

There is little or no evidence of FBAR being used aggressively against Americans abroad (at least yet). There are instances of FBAR being used aggressively against Homeland Americans who have deliberately failed to disclose foreign bank accounts for the purpose of evading U.S. taxes. (These were people who were considered to be

“bad actors“.)

FBAR penalties are not automatic …

The final paragraph of the

FBAR filing rules state:

This is consistent with the clear language in the

FBAR law. The law clearly encourages the filing of FBARs.

Mr. FBAR is admired and emulated …

The FBAR rules have recently been adopted by Russia and applied to Russian citizens. The penalties for noncompliance imposed by the Kremlin are NOT as severe as the penalties imposed by the IRS.

In any event, the FBAR filing requirement should be taken seriously.

*******

Part 1

As 2016 comes to an end …

Received #greatholidaynews today from two "ecstatic" renunciants who confirm that the wait time for CLNs is down to 2 – 3 months in Canada!

— Citizenship Lawyer (@ExpatriationLaw) December 17, 2016

I suspect that history will show that that the growth in renunciations

of U.S. citizenship (and abandonment of Green Cards) continued in 2016.

Absent a change in the way that the United States treats its “U.S.

Persons Abroad”, I suspect that the growth in renunciations will

continue.

The purpose of this post and a short summary …

This blog post will hopefully encourage those with U.S. tax issues to

consider whether they can deal with minor/unintentional FBAR violations

as a “stand alone single problem”. There may be no need to escalate and

expand one single problem into a multi-dimensional full blown tax

problem that may end up with unintended and unanticipated costly

professional fees as well as undue time spent! Read on and learn why.

Keeping a calm head is most important, even if it is most difficult to

do in the face of the scary situation of not being in compliance with

the U.S. tax and regulatory regime.

This post consists of the following six parts:

Part 1 – Problems, more problems and the expansion of

problems

Part 2 – Looking For Mr. FBAR

Part 3 – It often begins with a chance meeting with Mr.

FBAR

Part 4 – How the compliance problems of “Homeland Americans”

(particularly Green Card holders) differ from the compliance problems of

“Americans Abroad”

Part 5 – Focusing specifically on the problem of FBAR

non-compliance

Part 6 – Dealing with the tax professionals: Beware of how they

can expand the number of problems

_____________________________________________________

Part 1 – Problems, more problems and the expansion of

problems

For those who want to be in compliance with U.S. laws

…

It is my hope to encourage some thinking (“asking the right questions”)

and a calm (or calmer) state of mind. Obviously this post is NOT and

could NEVER constitute legal advice for you (or for anybody else). I

don’t know you. I don’t know your situation. But, I do want to share my

perception of why and how some very honest people ended up being

irreparably damaged by their attempts to “obey the

law”. Their attempts to “obey the law” were commendable. It was the way

that they went about attempting to “obey the law” that created the

problems. In many cases they started with an “FBAR problem”. They (or

rather their advisers) quickly expanded the problems and created a

costly compliance nightmare. It’s important for you to understand how

this happened.

For those who do NOT want to comply with U.S. laws …

This post is NOT directed to those who use “offshore accounts” to

facilitate tax evasion. (It’s unlikely that a person fitting this

profile would file FBARs anyway.)

But, what is/are the “laws” to which this post refers?

Recognizing that your goal is to “obey the law” …

At the risk of oversimplification, as a “U.S. Person” you must comply

with the rules of at least two separate U.S. statutes:

Title 31 – AKA “The law of Mr. FBAR”

Title 26 – AKA “The law of taxes”

It’s important to understand that Title 31 and Title 26 are separate

statutes with separate issues. They are logically unrelated!

Speaking of problems and the expansion of problems …

Let’s begin with the “John Richardson” principle of understanding and

dealing with “multiple problems”. It works like this.

Have you ever noticed the effect of compounding problems in your life?

Problems weigh you down? Say you start with one problem which weighs 10

pounds. If you get a second problem that weighs 10 pounds, the combined

weight (the way you feel it) is NOT 20 pounds. No, it’s more like 40

pounds. What if you add a third problem weighing 10 pounds? The combined

weight of the three problems is NOT 30 pounds. No, it’s more like 90

pounds.

Principle: The way that people experience the weight of

problems is this:

Anxiety/stress/distraction/weight of multiple problems = the the

square of the number of problems

Example:

Weight of 1 problem = 1 times 1 = 1

Weight of 2 problems = 2 times 2 = 4

Weight of 3 problems = 3 times 3 = 9

Notice that by solving one of the three problems, the weight

decreases by more than fifty percent. (Have you ever heard the

suggestion: Let’s do one thing at at time?) Notice also the compounding

effect of adding additional problems.

You need to understand the problem of allowing “single problems” to

escalate into “multiple problems”. This is critical when coping with

U.S. regulatory issues.

@ All

Seasonings Greetings!

Noticed Brock was pretty much Cloves’d for Christmas but hope everyone had a good Thyme.

Always grateful for the Sage posts and comments here and hoping FATCA relief is Cumin in the New Year.

From:

Rosemary, Basil, Ginger, Angelica, Cicely, Jimbu and Jasmine

PS — Yes, Angelica, Cicely, Jimbu and Jasmine are Allspice names.

@Embee, it was indeed the FBAR threat that terrified me into compliance, as many here know. It ultimately cost me over $10,000 in U.S. taxes, over $20,000 in accounting fees, and the loss of my birthright. :'(

I helped fund my accountant’s retirement.

“Seasonings Greetings!”

http://cheezburger.com/8996735488

@ monalisa1776

There simply are no words of consolation which can soften those heavy blows to your savings and being forced to relinquish your birthright. The unfairness of it all never diminishes.

I have what may very well be a stupid question but I’m asking it anyway. Let’s imagine that a US Person has a small mutual fund in the country he is living in, something the bank wanted to sell in exchange for a good mortgage rate, and the US Person was happy to do it to keep the bank happy and get the loan (the bank didn’t say anything about the US birthplace…). The US Person puts €100 per month on the account which now has a couple thousand euros on it and for all practical purposes it is a savings account. Along come the FBARs and that US Person decides to become compliant. He wants to file stuff to make the IRS and the USG happy. He also wants to file stuff that is truthful, but doesn’t want to go full compliance industry (he likes to make people happy, but there are limits). Here is the question. He writes down the mutual fund’s balance on the FBAR, but writes that it is a savings account and figures, probably naïvely, that this complies with the spirit of the law, all the while keeping things simpler and happier. Is that really stupid? Any cases concerning this kind of thing?

@ Fred

Sounds smart to me, as long as Bank hasn’t reported the savings account as being anything to the contrary, but if said person hasn’t had more than $10,000 in it I don’t think it would ring any bells.

BTW, congrats on making a wise decision re renunciation….. although I did find a New York in the UK!

https://en.wikipedia.org/wiki/New_York,_Lincolnshire

I have another idea. Don’t mention it.

Fred. Posted too quickly. Always keep firmly in mind: the IRS has no , repeat no, resources to go after minnows living offshore. They are underfunded understaffed and will have their funding cut further by the Con Don.

If you had a few hundred thousand euros in your account, you might have a problem. Otherwise forget about it.

@Embee, it was indeed life-altering. My situation was even worse because I’d already been filing so had to amend several years with all the dreaded PFIC calculations which resulted in all the U.S. tax. But at least my accountant was nuanced enough to keep me out of OVDI; she also enabled me to make a clean exit so I could renounce.

As John points out, I would have had more room to maneuver had I never filed tax returns. It’s cruelly ironic that my pen and paper efforts to be compliant created so many problems which escalated. Would have probably found a better result if I’d never filed… being in the system really put me into a corner, especially with the FBAR cudgel and with FATCA looming.

A quotation from the article is “The FBAR rules have recently been adopted by Russia and applied to Russian citizens.”

In fact it doesn’t apply to some non-resident citizens:

‘ – Russian nationals, including those temporarily living abroad or travelling as tourists, but excluding those living permanently abroad for more than one year; and

– foreign citizens who hold a Russian residence permit (“vid na jitel’stvo”).’

If a Russian national lives temporarily abroad, or permanently abroad for a permanent less than one year, they have to report Russian FBARs. We have to find out what they mean by temporary and permanent.

“He also wants to file stuff that is truthful”

He can’t. The IRS’s Taxpayer Advocate reported to Congress in 2011 that thousands of honest taxpayers were forced to renounce US citizenship because they couldn’t file stuff that is truthful. If you don’t like committing perjury, you have to renounce, but you’d still better commit perjury on the remaining forms you have to file in order to avoid penalties.

The IRS, Tax Court, Department of Justice, and Court of Federal Claims confirmed that the US properly penalizes honesty.

The IRS needs processable returns, where honest returns are not processable but perjured returns are.

26 USC sections 7206 and 7207 penalize wilful perjury but do not penalize coerced perjury. When the US coerces perjury, you’d better obey.

“Always keep firmly in mind: the IRS has no , repeat no, resources to go after minnows living offshore.”

Well, even if they have no resources for it, they are still fucking doing it. They still harass my wife, who was never even a US person, never had any US income, never had income higher than what the US would consider poverty level, and only made two mistakes: (1) marrying a (then) US citizen, and (2) signing my US tax returns when neither of us knew that honesty was illegal.

Why are US persons abroad silent on the unfairness of the US tax code towards US persons living abroad? Why 9m (or whatever the number is) are not protesting in front of the US embassies and choose to pay to overpriced tax specialists, overpay tax to the country they do not use any services in, jeopardise their retirement,etc? I understand that people who work for US companies abroad, are on assignments, etc – should file and comply with all this crap as they work for US companies, are abroad on temporary 1-2yr basis and will return. Why US citizens who chose to live abroad permanently due to personal reasons, live outside the US for 5-10-20-40yrs, do not work for US companies, etc still accept this barbaric practice of citizenship tax? Why is US government punishing its own people who have done nothing, but just chose to live abroad with double tax and excessive fines??? This is ridiculous. We need to make our voices heard by attracting media attention. Senators and Congressmen do not care and I doubt will ever introduce residence taxation (although this was stated in the GOP Better Way platform). The President does not care and initiated a war against own citizens who have done nothing wrong, only chose to leave their homeland and settle in foreign countries. We need to meet US ambassadors in our countries, start protests in front of the US embassies and attract attention of US media. Otherwise, we will end up overpaying tax without any real representation and use of any services. This is a servitude, not a democracy.

“Why are US persons abroad silent on the unfairness of the US tax code towards US persons living abroad?”

Well somewhere I saw a web site where some aren’t. There are also occasional articles on Forbes and a few in other radical traitorous sites such as Wall Street Journal.

But sure, why are 90% silent? Probably because they haven’t been caught yet and they figured out that they probably won’t get caught if they stay silent. They probably aren’t compliant either. They’re lucky enough to have a non-US birthplace in their passport (or maybe not even have a passport) and maybe really won’t get caught.

Among us few idiots who were compliant when we were US citizens, maybe it’s because we didn’t actually owe the US any money, we were used to the stress of spending 10 weekends each year trying to complete a few dozen forms, and we survived … until the IRS told us they were penalizing us for being honest.

Why are renunciations still counted in thousands instead of millions? Maybe millions won’t get caught.

P.S.

“own citizens who have done nothing wrong, only chose to leave their homeland and settle in foreign countries”

More commonly:

own citizens who have done nothing wrong, only chose to be born to parent(s) who had US citizenship

or:

own citizens who have done nothing wrong, only chose to be born in the US to parent(s) who were there temporarily

or:

non-citizens who have done nothing wrong, only chose to marry (oops this means they really did choose) a US person when they didn’t know what was coming.

Charlese1983 –

start protests in front of the US embassies and attract attention of US media

You are right … but.

Been there, chewed on that, many times.

Brock is populated with anonymouses who toe the curb.

Not what it takes to bell a facat.

Norman, that’s me and hubby to a T. We’re now faced with a terrible decision. We have no pension, never paid into US Social Security, and nothing whatsoever to support us in retirement except the rental from a property we bought ages ago. We’d like to sell that and put the money into something more high-yielding. There’s no capital gains tax where we live, but we all know that the IRS will stick its greedy fingers in. What with the gains both in value (after 18 years) and currency fluctuations, we stand to lose a major portion of our investment to the IRS if we sell, which devastates our retirement savings. So we are stuck. My husband now scolds me for having declared the rental income from our property, by which means the IRS is aware of it in the first place. Had we never mentioned it, maybe we’d have a chance to sell it “under the IRS radar”. Except for the fact that for a few hours our bank account will have a sudden surge in funds, and Mr FBAR will need to know.

I curse hubby in return for ever having been honest about filing our 1040s and FBARs starting when we moved abroad all those years ago. We can’t renounce unless we’re willing to go stateless. I want to cry my heart out right now.

Barbara, when I read these stories – I cannot believe what US does to its own citizens and the government believes this is normal. US citizens living abroad should protest this unfair servitude.

“I cannot believe what US does to its own citizens and the government believes this is normal. US citizens living abroad should protest this unfair servitude.”

I agree completely with the above statement, but have long ago come to the realisation that US citizens will never stand up for their rights or the rights of others who are discriminated against in their own country. The problem is that they are mostly cowards and unable to simply collectively refuse doing something that is so clearly and obviously unjust and discriminatory, even when it is against they themselves. You will never read anywhere on this site, or on any other, a general advice to simply not comply with these outrageous “laws”. No, quite the contrary, you will read long messages telling how to comply and what should be done to make things right. Enough of this nonsense! At what point do you simply say no and come and get me?

@ john

No, quite the contrary, you will read long messages telling how to comply and what should be done to make things right. Enough of this nonsense! At what point do you simply say no and come and get me?

you have not been around here long enough…..there are several long term brockers that are taking that exact tact……if perchance I were to get a brown envelope with from and amerikan 3 letter agency it would end up at the bottom of my bird cage……

people are fed up with the bully to the south and while the compliance complex is trying to instill fear into the people who are uninformed there is a growing movement of us who are saying enough and just not complying…….

@mettleman, as I do not have a pet bird I would have to buy maybe a hamster or gerbil and let it make a nest of it.

@John, “US citizens will never stand up for their rights or the rights of others who are discriminated against in their own country.” That future became clear on 9/11 when 99% of Amerika went shopping and 1% went to war, a war still ongoing paid for by borrowing money that will need to be paid by a generation not yet born.

@Barbara, I do not know you yet when I read your story there were honest tears in my eyes.

@Brockers, a quote from John McAfee the software guy….. “Rather than focusing on disrupting the bad guys in foreign countries, McAfee thinks that “all of that effort has been placed on a country that is afraid of its own citizens.”

I wonder what John McAfee would say about FBAR?

John, where did you get that idea? There is a sectionn on how to self relinquish and there are hundreds of posts suggesting less is better.

@ John and mettleman

If I had to guess at percentages I’d say, very roughly, 90% are hiding or dodging (knowingly or unknowingly), 9% (at an ever increasing rate) are complying and <1% are defying (some openly but most quietly because they don't participate in forums). This is just the sense of the situation I get from reading. Others may have a different take and better numbers. This doesn't look like the stuff and percentages needed to get a successful revolt going. There are a whole lot of people who aren't in the system. Koskinen hates them, he wants them in and he's out to get them. Compliance condors (with a few exceptions) drool over the pool of potential clients. Perhaps the tiny minority, the <1%, can grow a bit but, at this point, it doesn't look like it will be enough. Logos has left the building.

@dod, I appear to have misinterpreted the comment from John.

That said, we must be careful on the words that are used and I must say that “self relinquish” could be interpreted by non-friendlies as doing something not within the law.

A more appropriate term may be self documenting a lawful relinquishment. A CLN is NOT required to lose ones nationality and any attempt to require a CLN as a condition to lose ones nationality is a a violation of 8 US Code itself and the Expatriation Act.