Links to the FATCA debate in European parliament on FATCA.

European citizens versus the Borg

Links to the FATCA debate in European parliament on FATCA.

European citizens versus the Borg

Get your opinion delivered to President Trump: send it by Sept 30 to Expat’s POTUS-letter challenge at: taxreform@republicansoverseas.com

http://bit.ly/2fkikpw

Challenge 3 of your friends. And challenge them to challenge 3 of their friends.

This is the once-in-a-lifetime opportunity. Don’t blow it. Send it now. Let’s get rid of these unconstitutional impositions now

Our submissions should number in the thousands

“Republicans Overseas Action releases White Paper on Territorial Tax Reform for Individuals.

Consistent with the proposals being considered for corporate tax reform, worldwide taxation for individuals should be replaced with a territorial system. A territorial system for individuals would:

· Promote the exports of U. S. goods and services;

· Increase the soft power and reach of the U.S.

· Encourage skilled immigration to the U.S.

· Discourage expatriation of U.S. Citizens and encourage repatriation of wealth from overseas

· Eliminate unfair double taxation of U.S. Citizens

· Enhance U.S. national security by removing the sharing of sensitive personal information with unfriendly countries

· Substantially reduce the size and cost of the IRS

We welcome your comments and suggestions. Please email them to Ms. XXX at xxxx for our consideration and addition. We will ask Congress to consider our Territorial Tax Reform proposal for individuals. Happy New Year to all 9 million overseas Americans.”

// // // //

https://www.facebook.com/republicansoverseas/posts/606042006246265

Continue reading

U.S. expats come up short on many of the U.S. Bill of Rights. But their is some progress on of them, albeit one which much of the expat community doesn’t aggressively pursue–the 2nd amendment right “A well regulated militia being necessary to the security of a free state, the right of the people to keep and bear arms shall not be infringed.”

At issue, is whether a U.S. citizen has an equal and non-limited right to be armed while that U.S. citizen is in the U.S. The first discussion is that of an expat who holds a valid 2nd address in the U.S. The second discussion and case is related to an expat who has only a legal residence outside of U.S. The second case digs past a right which could be artificially be limited by the citizen’s uses, be it for sport or for self defense.

It’s not necessary for expats to enter into arguments as to whether this right is right or wrong, especially as this right is not shared in most of the countries where expats reside. In an effort to stay out of arguments as to whether this right is good or bad, just think of it as any one of any rights which might be granted by a constitution, which however is not afforded to non-resident citizens. Perhaps one could have a constitutional right to SuperSize Big Gulps, which may not be all that good for you or your family, but indeed it is a right which you might have to indulge in a product available to other resident U.S. citizens. The post is simply to point out only one effort to gain equal treatment for expats under the existing Constitution and its amendments.

THE PROBLEM STATEMENT

Federal laws prohibit non-residents of any/all states from purchasing arms throughout the country. An expat is a citizen with rights and those rights are not supposed to be infringed within the U.S. A U.S. citizen expat who can’t import a weapon and can’t purchase a weapon is then theoretically barred from exercising the right to bear arms as listed in the 2nd amendment (that is, if he isn’t required to borrow one from somebody (which is also probably currently illegal) or to have already “possessed” one prior to becoming an expat.

What is less relevant to most of the longterm “expat” or non-Homelander readers: The ATF issued an opinion in 2010 that essentially states a person can have two residences, one abroad and one in the U.S., and still be eligible to purchase a firearm in the U.S. during such times as the person occupies the U.S. residence. That opinion is at this link: https://www.atf.gov/file/55496/download.

“The Bureau of Alcohol, Tobacco, Firearms and Explosives (ATF) has received inquiries seeking clarification as to whether, under Federal law, United States citizens who maintain residences in both a foreign country and a particular State may purchase firearms while in the State.

ATF has previously addressed the eligibility of individuals to acquire firearms who maintain residences in more than one State. Federal regulations at 27 CFR 478.11 (definition of State of Residence), Example 2, clarify that a U.S. citizen with homes in twoStates may, during the period of time the person actually resides in a particular State, purchase a firearm in that State. See also where ATF held that, during the time college students actually reside in a college dormitory or at an off campus location, they are considered residents of the State where the on campus or off campus housing is located.

The same reasoning applies to citizens of the United States who reside temporarily outside of the country for extended periods of time, but who also maintain residency in a particular State. Where a citizen temporarily resides outside of the country, but also has the intention of making a home in a particular State, the citizen is a resident of the State during the time he or she actually resides in that State. In acquiring a firearm, the individual must demonstrate to the transferorlicensee that he or she is a resident of the State by presenting valid identification documents.

Held, for the purpose of acquiring firearms under the Gun Control Act of 1968, a United States citizen who temporarily resides in a foreign country, but who also demonstrates the intention of making a home in a particular State, is a resident of the State during the time period he or she actually resides in that State.

Held further, the intention of making a home in a State must be demonstrated to a Federal firearms licensee by presenting valid identiication documents. Such documents include, but are not limited to, driver’s licenses, voter registration, tax records, or vehicle registration.

RIGHTS FOR NON RESIDENTS

More relevant to most readers is that federal law effectively blocks the purchase of a firearm in the U.S. by a U.S. citizen living abroad with no residence in the U.S.

The federal ban is the subject of a long-running Second Amendment challenge, currently captioned Dearth v. Lynch. The most recent published opinion in that case, from June 2015, denied the government’s request for summary judgment and remanded the case for trial.

In the arguments (whose language and logic is partially understandable), it was established that the plaintiff indeed had no options available to him as a U.S. citizen to bear arms in the United States. The case looked at his potential ability to import a weapon, which he could not. It also looked at the various state/federal laws that may have allowed him to have firearms for sporting purposes, but the court found that there was no documented method of purchasing firearms for other legally valid purposes (self defense). It also appears to throw out any thoughts that it is states that should be the plaintiff, and it finds that there indeed states which do not prohibit non-resident purchasers, but it is indeed federal law that prevents the plaintif from purchasing the weapon for which his constitution states should not be limited,

The case illustrates that indeed, it has been fully possible for a combination of state and federal laws to prevent the exercise of non-resident citizens from exercising their Constitutional rights. Also, that the possibility of seeing the proper court does exist if one has access (including financial) to lawyers with sufficient expertise. It also points out the long road necessary to even reach a court which might make a decision.

http://caselaw.findlaw.com/us-dc-circuit/1705364.html

Animal Farm – Wikipedia, the free encyclopedia// //

“All animals are equal but some animals are more equal than others”. George Orwell

(Again, this author does not enter the argument as to whether the 2nd amendment is a good right or a bad right.)

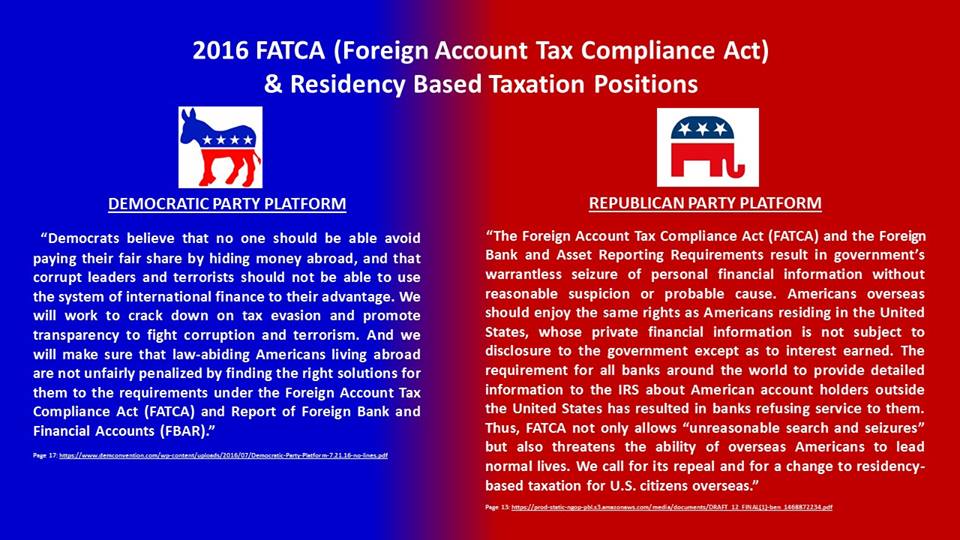

The platforms listed side by side ties expats with either fairshare/terrorism/corruption/criminality/evasion/cracking down whilst the other focuses upon constitutional rights and the ability for overseas Americans to lead normal lives. Consider the expat-relevant platforms in regards to the Congressional and Presidential choices.

(No relevant information found yet from the Libertarian or Green party)

The platform gives direct information as to what the two parties think of us.

Here is the Hillary position

http://www.democratsabroad.org/our_candidates#Hillary

For The Hillary’s personal message, go to this Brock post

http://isaacbrocksociety.ca/2016/07/03/fourthofjuly-independenceday-analysis-the-fastest-growing-u-s-state-lies-outside-its-borders/

If there is a message from the RNC candidate Trump, we can compare it here

GAO begins doublespeak already in the title “Economic Benefits of Income Exclusion for U.S. Citizens Working Abroad Are Uncertain ” The entire report –investigating removal of the FEIE “tax expenditure” reads like the script of 1980’s shortwave Radio Moscow—full of “some experts say” and “it can’t be shown” doublespeak. Already on the 1st page “GAO made no recommendations in this report.” . GAO doublespeak already says that “uncertain” in its title means it has “No recommendations.” The table of contents itself is full of doublespeak conclusions.

In order to fully understand what the 74 page General Accounting Office (GAO) report is saying, one really needs to have fluency in doublespeak—-to grasp the real meaning. For those who can read doublespeak, this report might best be read alone in that quiet place after having your morning coffee. Otherwise, I will attempt to provide a translation.

May 20, 2014, The Honorable Jim McDermott, The Honorable Michael Honda. The Honorable Carolyn Maloney, House of Representatives

Apparently the report was commissioned by the well-meaning, yet passively-aggressively naive Abroad Caucus, in response to repeated visits by ACA/AARO.

The immediate cause of the caucus naive error is in commissioning the study to G.A.O. –the General Accounting Office. This band of merry men has a self-interest in making as much form filing work as possible, even though its extra-territorial taxation method might never create any tax revenues.

GAO then went on to interview the normal lackeys “government officials, experts, and stakeholders, including groups representing citizens working abroad and employers”. The list (described in Appendix 1) is stacked with “experts” in creating complicated compliance law in their own interest. The last on the list is American Citizens Abroad who has been profiling itself as “THE Voice of Americans Overseas” . AARO with a similar approach. As we know, there are still no other expat organizations than these two 40-yr-old organization

As the biases are built into the report by its authors and experts, it understandably comes up with a list of options in Appendix 1, Table 7, which range from worse to bad:

-Repeal the FEIE & tax all foreign earned income.

-Reduce the maximum exclusion

-Increase the maximum exclusion

-Restrict eligibility,

-Expand eligibility

-indexed for the cost of living.

– convert the exclusion to a credit

-targeted to employees of selected industries. —(oil & gas, construction, engineering, UN work)

-Uncap the exclusion and exclude all foreign earned income from taxation (but not enact RBT).

-Impose an exit fee on U.S. citizens and U.S. resident aliens living in a foreign country & exclude all foreign income for eligible individuals living overseas (ACA proposal).

Continue reading

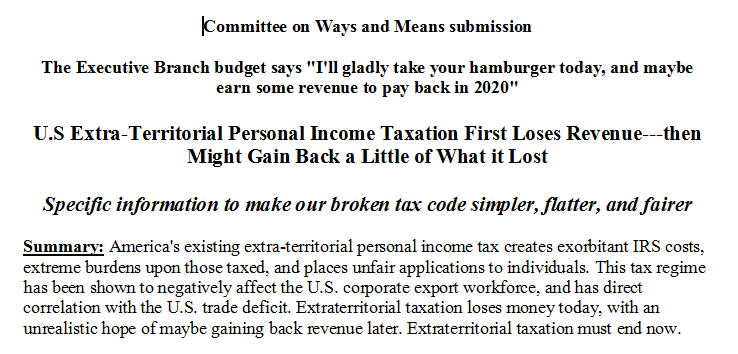

The Executive Branch budget says “I’ll gladly take your hamburger today, and maybe earn some revenue to pay back in 2020” —-it definitely won’t be paying back on Tuesday.

This submission was made by a guest and based upon many posts in Isaac Brock. Its author hopes to be called to witness or hopes that press might pick up the information that the U.S. govt is getting duped by their own bureaucracy into the exorbitant current costs of implementing extra-territorial taxation–in pursuit of rainbows and while fighting windmills. We also hope that the press will notice the quantity of our submissions.

Please send in YOUR submission today. Two lines, 2 paragraphs, 2 pages—anything. Tell them that the consumption tax is great, the flat tax (as written) is disastrous, and that CBT must be eliminated immediately. You have the rest of today according to Washington D.C. (Eastern) time. Submission instructions are in previous post.

Please submit to Ways Means. One line. One paragraph. One page. One dissertation. Whatever.

ADDTIONAL NOTE: THE HEARING IS BASED UPON REDUCING IRS PAPERWORK and gives 2 means to potentially achieve that end. FOCUS YOUR COMMENTS UPON REDUCTION OF COMPLEXITY and cost savings in eliminating paperwork. Also, payment for services rendered such as the consumption tax they mention.

EXPRESS SUPPORT FOR CONSUMPTION TAXES and disgust for flat taxes which would devastate us.

Quantity of Responses should overwhelm the discussion. There should be no excuses for Ways Means to not address it.

http://waysandmeans.house.gov/boustany-announces-hearing-on-fundamental-tax-reform-proposals/

Public Submissions For Record

Please click here to submit a statement or letter for the record

WASHINGTON, D.C. – House Ways and Means Tax Policy Subcommittee Chairman Charles Boustany (R-LA) announced that the Subcommittee will hold a hearing entitled “Fundamental Tax Reform Proposals” on Tuesday, March 22nd at 2:30 PM in room 1100 of the Longworth House Office Building. This will be the first in a series of hearings where members of both parties will have the opportunity to share, discuss, and promote their proposals for tax reform. The particular focus of this hearing will be legislative proposals presenting cash-flow and consumption-based approaches to taxation.

Upon announcing the hearing, Chairman Boustany said:

“Chairman Brady has laid out a strong vision and set of policy goals for making our broken tax code simpler, flatter, and fairer. Tax reform represents a crucial part of our party’s pro-growth agenda, and I am committed to accomplishing these goals by considering bold, new ideas and building consensus among our members. Next week’s discussion will give my Ways and Means colleagues and me the opportunity to take a closer look at the forward-thinking proposals for tax reform that our members have developed.”

Let’s recognize in advance that there are many on this site who are not willful U.S. citizens, but let’s hope that the repeal segment of readers can step up to the plate.

remember FOLLOW INSTRUCTIONS: All submissions must include a list of all clients, persons and/or organizations on whose behalf the witness appears. The name, company, address, telephone, and fax numbers of each witness must be included in the body of the email. Please exclude any personal identifiable information in the attached submission.

If not, submission is dismissed.

If America truly wanted to tax “rich” expats–expats would simply be taxed upon any income over $x00,000 yearly income at some rate, whilst others would imply not file. Although this method would still be taxation without providing government services, it would at least be honest about only ripping off expats who are “rich”. That method would have been recommendable by any lousy government official after reading my last entries.

After analyzing 86.7% of the expat/emigrant population in those articles, it shows that only maximum 0.293% would owe tax to US according to the principle of “taxing-up” to the higher of residential tax or homeland USA tax, using the existing method of exclusions and credits. But even this level of unexcellence is unachievable to that Washington leadership that doesn’t represent us.

The preceding calculations are made under an assumption that the exclusion/credit process is clean. But it isn’t. We’ve long discussed all the form complexity manufactured by the compliance mafia which rotates in and out of Treasury employment. The mafia has made the paperwork of an expat to be more than double that of a homeland tax return. And, whereas homelanders can have their taxes done by low/moderately priced bookeepers, expats must have their taxes done by $200 / hr accountants.

The compliance mafia has also written in an infinite number of reverse loopholes—where, at every turn, the IRS has an opportunity to screw a taxpayer using the complexity of the rule system. We’ve discussed many of these reverse loopholes at this site in these years. Please feel free to throw in your own.

-PFIC’s–the nightmare–any fund product not purchased in America will be taxed enough to rid the person of any profits

– Double taxation of foreign social taxes. For example, in Norway, the social tax is listed separately from other taxes. Social taxes are not creditable or deductible, hence America double-taxes it.

– Double taxation of renunciants: The exit tax (reichfluchtsteuer) was supposedly designed to capture the capital gains of a human being over its life as an American. If that American had always lived in America, the exit tax might represent a clean (bad) tax. But, a human being living out its life outside of America is already due those capital gains taxes to the country of his residence. The reichfluchtsteuer taxes the gains due to his existence as an American, and the American is later taxed honestly by his country of residence, too. ……… and the list goes on….

These reverse loopholes were left out of the analysis, because their effect upon America’s tax revenue is negligible. The issue to note especially in this article, is that these reverse-loophole taxes are destructive upon the individuals they land upon. These stupid reverse loopholes are what make it impossible for Americans to have financial planning if not living in the homeland.

The IRS and the compliance mafia have been happy to force non-rich expats to file mounds of paper, to punish particular persons with obscure rules, to force Americans to exclude or credit things for which they never should have been charged, and then to create ethnic discrimination tools such as FATCA to enforce bad rules. All of this effort has been made by the IRS and compliance condors to grab money they never deserved, with with even lesser significant revenue than the tax revenue I have been showing in previous calculations.

With that clarification, it should be possible to continue with the calculations.