CRA and IRS hand-in-hand

John Richardson, with the Alliance for The Defence of Canadian Sovereignty, discusses the impact of the controversial 2014 FATCA IGA tax deal on U.S. citizens living in Canada. John is interviewed by CBC’s Dianne Buckner.

CRA and IRS hand-in-hand

John Richardson, with the Alliance for The Defence of Canadian Sovereignty, discusses the impact of the controversial 2014 FATCA IGA tax deal on U.S. citizens living in Canada. John is interviewed by CBC’s Dianne Buckner.

Posted on Ipolitics.ca You can add your comments at that website. The title of the article is “Revenue Canada quietly handed 155,000 Canadian banking records to IRS”

[Note that the journalist began article with point that our Canadian Government sent private bank info south before receiving privacy assessment from Office of Privacy Commissioner. Journalist failed to find Liberal Government MP willing to chat but did hunt down Liberal Senator who complained about actions of the Tories.]

The journalist, Elizabeth Thompson, comments on her own article: “The language is not misleading. A number of people I interviewed told me of their efforts to get comments from the new Liberal government since the election – from the same Liberal MPs who commented on this issue before the election. I’m trying once again today for an interview with the Revenue Minister (who has a lot less to do with the budget than the finance minister does) and I will keep trying.”]

THE ARTICLE:

“The Canada Revenue Agency quietly turned 155,000 banking records over to the U.S. Internal Revenue Service during last fall’s election, without waiting for an assessment from Canada’s Privacy Commissioner or the outcome of a court challenge to the controversial move.

Hillary prevented IRS from gaining access to more than 91% of illicit, tax-evading UBS offshore accounts. https://t.co/0yH91u4Hly

— Patricia Moon (@nobledreamer16) March 12, 2016

This story appeared in The Hill on Friday, March 10, 2016. I simply cannot believe I have not heard anyone in the expat world speak of it, and/or the American presidential arena has failed to emphasize it. Perhaps it is just buried along with the general theme of Ms. Clinton, her Wall St. speeches and “her damn emails.”

Everyone would agree that it is the fault of the Homelanders with Swiss bank accounts who caused the disruption in the way of life as we know it, wouldn’t we? We all went about our lives, blissfully unaware of the creeping edge of unenforced CBT until 2008 when the IRS and DOJ found a way to go after the real tax evaders. First came the unending threats of then-Commissioner Douglas Shulman regarding “our last best chance,” endless media blithering about “coming clean” and the very real life-threatening FBAR penalties…OVDP/OVDI and well, you know the rest of the story.

And we all have heard the justification that the laws have to be applied as they are because as unfortunate as it is that we are affected, (unintentionally, ja right) no party can come out and endorse such changes because they would be seen as supporting tax evasion, right?

Well Madame Secretary Clinton has bested that by a long shot. It is so outrageous you simply cannot make this kind of stuff up.

In March 2009, after meeting with Swiss Foreign Minister Micheline Calmy-Rey, then Secretary of State Hillary Clinton intervened with the U.S. Internal Revenue Service (IRS) on behalf of Switzerland’s most powerful banking institution, UBS. The IRS, which at that time was seeking the identity of wealthy Americans who had stashed some $20 billion in 52,000 tax evading UBS accounts, then agreed that the Swiss bank need only turn over information on 4,450 accounts. Afterwards, UBS increased its previous $60,000 in donations to the Clinton Foundation ten-fold. By the end of 2014, UBS donations to the Clinton Foundation totaled $600,000. UBS also “paid former President Bill Clinton $1.5 million to participate in a series of question-and-answer sessions with UBS Wealth Management Chief Executive Bob McCann, making UBS his biggest single corporate source of speech income disclosed since he left the White House.” ……

***

When UBS, which could have lost its ability to conduct business in the U.S. if successfully prosecuted, balked at the IRS demand that it turn over information for all 52,000 accounts, the IRS filed a legal action seeking to compel disclosure. That is when, at the behest of the Swiss government, Hillary Clinton stepped in to negotiate a deal that prevented the IRS from gaining access to more than 91 percent of the illicit, tax-evading offshore accounts.

The Hill article is rather short with few links and nothing much to back up these claims. So I spent the afternoon researching this and it has been in the news all along and is not even remotely mysterious. And it forms part of the longer narrative which demonstrates so clearly that the Clintons are most certainly not the candidates for everyday people. Watching these Town Hall Meetings where regular folks get up and are all starry-eyed about actually getting to ask a question reminds me of the looks on the Trudeau cabinet last week in DC. And it would truly be in the best interests of the entirety of the American people to realize just how much the tax debt remains an affair of the wealthy-that they, the banks and their candidates are taking every dime they can away from the little guys.

Continue reading

If America truly wanted to tax “rich” expats–expats would simply be taxed upon any income over $x00,000 yearly income at some rate, whilst others would imply not file. Although this method would still be taxation without providing government services, it would at least be honest about only ripping off expats who are “rich”. That method would have been recommendable by any lousy government official after reading my last entries.

After analyzing 86.7% of the expat/emigrant population in those articles, it shows that only maximum 0.293% would owe tax to US according to the principle of “taxing-up” to the higher of residential tax or homeland USA tax, using the existing method of exclusions and credits. But even this level of unexcellence is unachievable to that Washington leadership that doesn’t represent us.

The preceding calculations are made under an assumption that the exclusion/credit process is clean. But it isn’t. We’ve long discussed all the form complexity manufactured by the compliance mafia which rotates in and out of Treasury employment. The mafia has made the paperwork of an expat to be more than double that of a homeland tax return. And, whereas homelanders can have their taxes done by low/moderately priced bookeepers, expats must have their taxes done by $200 / hr accountants.

The compliance mafia has also written in an infinite number of reverse loopholes—where, at every turn, the IRS has an opportunity to screw a taxpayer using the complexity of the rule system. We’ve discussed many of these reverse loopholes at this site in these years. Please feel free to throw in your own.

-PFIC’s–the nightmare–any fund product not purchased in America will be taxed enough to rid the person of any profits

– Double taxation of foreign social taxes. For example, in Norway, the social tax is listed separately from other taxes. Social taxes are not creditable or deductible, hence America double-taxes it.

– Double taxation of renunciants: The exit tax (reichfluchtsteuer) was supposedly designed to capture the capital gains of a human being over its life as an American. If that American had always lived in America, the exit tax might represent a clean (bad) tax. But, a human being living out its life outside of America is already due those capital gains taxes to the country of his residence. The reichfluchtsteuer taxes the gains due to his existence as an American, and the American is later taxed honestly by his country of residence, too. ……… and the list goes on….

These reverse loopholes were left out of the analysis, because their effect upon America’s tax revenue is negligible. The issue to note especially in this article, is that these reverse-loophole taxes are destructive upon the individuals they land upon. These stupid reverse loopholes are what make it impossible for Americans to have financial planning if not living in the homeland.

The IRS and the compliance mafia have been happy to force non-rich expats to file mounds of paper, to punish particular persons with obscure rules, to force Americans to exclude or credit things for which they never should have been charged, and then to create ethnic discrimination tools such as FATCA to enforce bad rules. All of this effort has been made by the IRS and compliance condors to grab money they never deserved, with with even lesser significant revenue than the tax revenue I have been showing in previous calculations.

With that clarification, it should be possible to continue with the calculations.

New Zealand’s financial industry invested 100 million NZD, whilst its government invest 20 million NZD to prevent Americans from sending their money to New Zealand to avoid taxation. Also, eligible Kiwis can be identified to pay tax to USA–to help USA tax Kiwis whom USA declares “United States Persons for Tax Purposes“. Such identified Kiwis can be forced to pay U.S. taxes while living in Kiwiland.

So far, by investigating the highest two US tax categories, we’ve seen that the only 0.274% of the first 81.1% of the expat population’s tax returns yield tax revenue to USA. Now, we investigate expats who may be exposed to USA’s 33% to 35% tax bracket—which comprises 1.9% of the US expat population. If a United States person lives in a country in this range, he could be exposed to USA taxation ranging from 0% all the way up to 6.9% (average 3.45%). These countries are identified to have taxes in this range (with percentages of the US expat population).

Total 1.9%

Colombia 0.7%

Guyana 0.0%

New Zealand 0.8%

Swaziland 0.0%

Venezuela 0.4%

New Zealand is the most significant in this group, and has a top marginal tax rate of 33%. Let’s compare that to America’s tax tables.

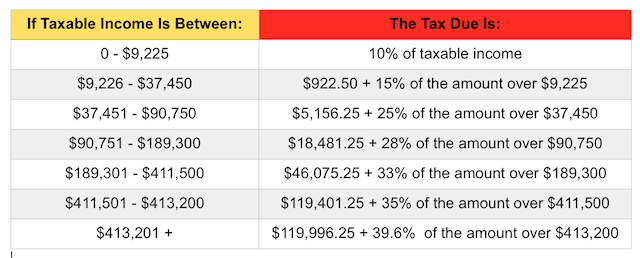

U.S. tax rates for single filers

America has a policy to require its citizens to pay additional tax to U.S.A. if the residence country of a U.S. citizen is not as high as the U.S. tax rate. It has about a $100,000 income exemption. Hence, a US person in New Zealand making 511,501 USD to 513,200 USD per year will be taxed by USA an additional 2% (a very narrow band worth considering insignificant). For any income above $513,201 USD, USA will tax that person 6.9%. This means, that USA can only tax dual citizen Kiwis with incomes over $513,201 (763,000 NZD).

So, how many Kiwis have incomes over 763,000NZD? A: Far less than 1% of the Kiwi population, or less than 1% of the dual-citizen population.

New Zealand has 0.7658% of the US expat population. And therefore, less than 0.07658% of the U.S. expat population can be taxed 6.9% of their marginal income above $513,200. This is beginning to sound ridiculous–Just BEGINNING to sound ridiculous. The story can be no better than U.S. citizens living in Colombia (0.7%), Guyana (0.0%), Swaziland (0.0%), or Venezuela (0.4%). Less than 0.019% of the US expat population can be taxed maximum 6.9% for their incomes above $513,200.

In New Zealand—how many people is this really? Various estimates yield the quantity of U.S. citizens in New Zealand to be between 21,462 Kiwis BORN in USA, to 38,207 to 66,600 Kiwis with known and unknown US citizenship. USA could tax less than 1% of them.

USA could potentially tax less than 666 Kiwis 6.9% of their marginal income above $513,200.

The ridiculousness of America’s extra-territorial taxation glares in New Zealand.

New Zealand has self-paid more than 120 million NZD to help America collect taxes from less than 666 rich dual-citizen Kiwis.

No matter how much money the IRS will lose, the IRS, Washington, and mainstream media want to tax US expats. The IRS and Washington want a government jobs program for accountants in the public and private sectors. And FATCA is the enforcement tool of USA’s stupid extra-territorial personal income tax system of Citizenship-Based-Taxation (CBT) (or US-person Based Taxation).

Note that USA and Eritrea are the only governments of the world that tax their expatriates and emigrants. But is USA making any money (tax revenue) out of the effort?

America’s first goal is to use U.S. expat citizens to fund the U.S. tax-preparer industry. A typical taxpayer is required to pay about $500 a year to hire a U.S. tax professional to fill out expat tax forms that are exponentially more complicated than tax forms for Homelanders. USA wants for the entire adult (over 25 yrs) U.S. expat population to pay for this. So, the compliance industry is fleecing the citizenry right good–a wealth transfer from those of modest means to tax preparation corporations (so what else is new?). But is the IRS gaining revenue?

We can look at what IRS costs are incurred, assuming that the IRS is successful in forcing every tax-eligible expat to file. The IRS is able to estimate the cost of each filer–unfortunately the IRS does not share those numbers with the public (it would defeat its self-serving job-security interest). Note that expat returns are at least doubly complicated than those of homelanders. Normally, the poor would be relieved of their need to file–-but with Obamacare, even the poor are required to file expat exemption papers. For example, expats can never be eligible for Obamacare, yet expats who file must file a form to exempt themselves from Obamacare penalties. Hence, it is likely that the entire adult expat population will file forms which can give IRS job security. 56% of the world are adults above 24 yrs, and there are 8.7 million U.S. expats. One could expand the analysis to try to determine the number of “US persons”, but this article will limit the scope to US citizen expats. (8.7 million)(0.56)* (processing cost of one filer)(doubled)(% above filing threshold).

In addition, there is a similar-but-different population of FBAR filers to consider. Each FBAR of every account of every expat who possesses more than $10,000 of financial wealth must also be processed. These FBARs must be filed and compared to the data which is obtained through the FATCA ethnic-identification system. FATCA’s public costs could also be considered in the calculation–FATCA is a big loser to the world’s economies. FATCA’s costs to the IRS government system are partly addressed in Wikipedia. However, “The I.R.S. “has been unable to ascertain all potential costs beyond those for IT resources”.

It’s important to remember that, despite media propoganda, FATCA and FBAR are not taxes and do not create tax revenue. They are expensive unconstitutional enforcement means of the money-losing extra-territorial tax regime system. Although sold to the public as revenue-enhancers by “increasing tax revenues”, enforcement methods and control systems always only add costs. This government doublespeak shows up in every Congressional spending bill (correctly stated as not a tax) but as “revenue enhancement”.

But does America’s extra-territorial taxation system take in any money? If America succeeds with its FATCA and finds ALL of its 8.7 million expat-chattel in the world, how many dineros will it bring to itself? Let’s calculate some examples using IRS tax tables.

53.7% of US expats live in countries which have higher marginal tax rates than USA’s top 39.6% rate. No matter what their income, US cannot tax them up. More than half of the people filing expat taxes should (rightly) owe nothing. Zilch. Zippo.

27.4% of US expats live in countries with tax brackets in the 35% to 39.6% region. With USA’s taxing-up method, it could gain a maximum of 4.6% tax (average 2.3%) from the richest of any residents. But a single person must make over $413,200 per year to pass this 35% marginal-tax threshold—however that person can exclude at least $100,000, so a person must make more than $513,200 per year to be taxed in this bracket. The only significant country in this category is Mexico, where 52.3% of the population is below the poverty line and 90% earn less than $33,000 per year. In order for America to get any money out of Mexico, they would have to fleece Mexico’s 1%’er’s . So, in Mexico, more than 99% of the US-expat tax filings would be wasted energy. To know how much money America could squeeze out of Mexico, one would have know the percentage of 1%ers who are dual citizens. The quantity of Mexican US persons to be taxed becomes negligible.

The other cash cows in this category include Algeria, Argentina, Cyprus, Ecuador, Morocco, Norway, Thailand, Turkey, and Vietnam. How many Turks or Argentinians could America fleece? (oops, side point: I forgot to mention that the IRS disallows tax credits for the Norwegian 7.8% tax it labels “social tax”. The IRS wrongly taxes Norwegian residents due to a loophole it wrote into tax treaties and tax regs)

Ok, so we’ve gone through 81.1% of the expat population’s tax returns — and the only thing that has been achieved is that 80.826% have (rightly) contributed no tax revenue to USA and less than 0.274% may have (unrightly) been taxed-up by USA by a tax ranging from 0% to 4.6% of their annual incomes. Oops, I forgot — only 56% of that population are adults. This whopping sum ought to pay for a few dozen aeronautical toilet seats.

I hope that you are beginning to see the ridiculousness of the situation. The GAO has full access to this type of data, and should have been able to calculate this same data. They should have been realizing that the costs of processing millions of returns is ridiculously high in comparison with the ridiculously low revenue potential to be gained from fleecing the 1%’er expats in Algeria, Norway, or Vietnam.

Well, politics is an endless source of black humor. You ought to know that the story just gets more and more ridiculous if one analyzes it further.

America’s extra-territorial US-person-based taxation (CBT) is a big big loser for America. And CBT helps even more to show that the taxing decision makers in Washington are truly a bunch of losers.

Ben Steverman, a reporter for Bloomberg (New York), is preparing a personal finance article on special tax issues that expat lambikins face as they file US taxes from outside the jurisdiction of the USA. He understands these lupine tax obligations have become increasingly aggravating and expensive.

Interested lambikins should contact him before Monday when he hopes to conduct his interviews. He can be reached at his bloomberg.net email address, (bsteverman@).

See below March 9, 2016 response of new Liberal Canadian Government to January 21, 2016 FATCA questions raised by NDP Revenue Critic Mr. Pierre-Luc Dusseault (Sherbrooke).

Response comes from Canada Revenue Agency, Minister of National Revenue (who we are suing), Finance Canada, Stephane Dion, and Attorney General (who we are also suing).

SEE THE LINK. The text is in both english and french.

Bottom line: 1) We are still second class — our lawsuit continues; and 2) WE NEED MORE WITNESSES.

— I am amazed that the Prime Minister of Canada allowed this statement to be included in the response, asking Canadians to recognize the public interest of the United States at the expense of the sovereignty of our country:

“…we must resign ourselves to the fact that we are faced with a requirement from the United States and that the requirement corresponds to the public interest of the United States, meaning the integrity of their tax regime.”

— The OPC privacy review was passed on to CRA in January 2016 AFTER the September 2015 turnover of your bank records. In other words, Canada does the privacy assessment AFTER the turnover of private confidential data. See below statement:

“Part (aa): The CRA consulted with the Office of the Privacy Commissioner (OPC). A privacy impact assessment (PIA), which is a policy process for identifying, assessing, and mitigating privacy risks, was completed and submitted to the OPC for review on August 27, 2015. The CRA received the OPC’s recommendations on January 4, 2016 [AFTER THE TURNOVER]. The recommendations do not prevent the CRA from exchanging the required information. A response to the OPC’s recommendations is being prepared.”

Mr. Dusseault is now considering his next step. If you have follow-up questions you would like him to ask Mr. Trudeau (e.g., “…But Mr. Trudeau, what about that pre-election statement you made that Canada’s FATCA IGA legislation is insufficient to protect Canadians? What changed your mind?”) you can email him at Pierre-Luc.Dusseault@parl.gc.ca

United States Secretary of State John Kerry offers this accurate assessment of Prime Minister Justin Trudeau: “It’s clear that the Prime Minister has begun to make his mark on Canada’s future.”

USCitizenAbroad comments on Government response:

Taxing Away Citizenship: Do American-Canadian dual citizens consider their status to be an inconvenience?

by

James Eastman-Timmons

A thesis submitted to the Faculty of Graduate and Postdoctoral Affairs in partial fulfillment of the requirements for the degree of

Master of Arts

in

Sociology

Carleton University

Ottawa, Ontario

©2015

James Eastman-Timmons