This post is from the RenounceUScitizenship blog.

Citizenship-based taxation – Residence based life control

All U.S. citizens abroad are living the reality that the tax and reporting requirements of U.S. citizenship abroad have meant that U.S. citizenship has been priced out of the market. Many U.S. citizens abroad simply do NOT have the money to pay the compliance costs. Furthermore, it has become clear that what the U.S. refers to as “citizenship-based taxation” is actually a deliberate form of “residence based life control“. Let’s at least understand what we are talking about.

The role of the IRS – “It’s about the control stupid”

As you know the IRS is working hard to extend its regulatory reach over all aspects of tax compliance. Attorneys, CPAs, EA, and anybody else (whoever that might be) are already subject to IRS Circular 230. In simple terms: this means that their livelihood is subject to compliance with IRS rules. It has reached the point where many believe (with justification) that the the tax professionals are a greater threat to U.S. citizens abroad than the IRS could ever be.

Recently the IRS has attempted to:

1. Impose licensing requirements on all tax preparers; and

2. Require “tax preparers” to pass an IRS licensing exam.

As I once tweeted:

There is a big difference between tax preparers being regulated as a general principle, and tax preparers being regulated directly by the IRS.

There are many reasons why as a matter of principle and policy the IRS should not be permitted to impose a licensing requirement on tax preparers. At least for the moment, the courts agree. Pending the usual appeals process, a court has struck the requirement down.

HR Block is a huge beneficiary of IRS regulation of tax preparers!

Put it another way:

Although the IRS and the compliance industry are business partners, HR Block is a preferred partner!

As I noted in a previous post on the IRS regulation of tax preparers:

The effect of all this on “small preparers” was described by Bloomberg:

“UBS AG analysts Andrew Fones and Margaret O’Connor issued a report that said the IRS initiative will help H&R Block by preventing small preparers from entering the market and driving others out of it.

“We think the regulations could be a boost for Block starting” in 2011, the analysts said.”

It is in effect a “tax” on “tax”. Yes, that is where the U.S. has come to . The additional costs of having your tax return completed, are a tax on tax itself. But I digress.

So, it is in the interests of the big boys “HR Block”, etc. to have barriers to entering the tax preparation business. Now, the story continues to get even more interesting (and this may all be only circumstantial and irrelevant). But, it is very interesting. The Washington Examiner opines that:

“But again, H&R Block isn’t just a passive beneficiary of this regulation — it was an active supporter. In July, once the IRS announced it was considering these rules, H&R Block hired the Podesta Group to lobby on the matter. The Podesta Group was co-founded by John Podesta, who later became an Obama confidant and his transition director. Podesta Group is currently run by Tony Podesta, the leading lobbyist-bundler in the country, who has raised, together with his lobbyist wife, well over half a million for Democrats this election.

But wait, it gets better. The IRS official in charge of writing these rules: Mark Ernst, former CEO of H&R Block. As I wrote at the time:

Mark Ernst, in December 2007, was chief executive officer of H&R Block, the nation’s largest tax-preparation company. Thirteen months later, once President Obama took office, Ernst was named a deputy commissioner at the Internal Revenue Service, where he would spend his first year drafting new regulations for tax preparers — regulations that H&R Block welcomes and market analysts say will benefit the company.

With Ernst in mind, recall Barack Obama’s campaign pledge: “No political appointees in an Obama administration will be permitted to work on regulations or contracts directly and substantially related to their prior employer for two years.”

This campaign pledge manifested itself in an executive order requiring “every appointee in every executive agency” to pledge, “I will not for a period of 2 years from the date of my appointment participate in any particular matter involving specific parties that is directly and substantially related to my former employer or former clients, including regulations and contracts.”

Ernst obviously didn’t follow these rules, but the IRS tells me that Ernst is not covered by these rules. “Mark Ernst is a civil servant at the IRS; he is not a political appointee,” according to an e-mail IRS statement by an agency spokesman.”

Mark Ernst became a deputy IRS commissioner in early 2009.

Now, just in case you are not getting this:

- HR Block is one of the principal beneficiaries of the IRS tax regs

- There is evidence that HR Block lobbied to get these regs passed

- Mark Ernst who was the CEO of HR Block from 2001 – 2007 became a deputy commissioner of the IRS. In that role, he may have been responsible for assisting with the development of the IRS rules and regulations governing the tax preparation industry.

Does this pass the smell test? Is there anything wrong with the former CEO of HR Block becoming a deputy commissioner at the IRS? I don’t know. You tell me.

Epilogue:

Mark Ernst’s tenure at the IRS did not last long (early 2009 to late 2010). As noted by “Accounting Today”

“IRS Deputy Commissioner Mark Ernst Resigns

Washington, D.C. (October 21, 2010)

By WebCPA Staff

Mark Ernst, the former chairman and CEO of H&R Block who went on to become deputy commissioner for operations support at the Internal Revenue Service, will be leaving the IRS later this year, according to an announcement Thursday by IRS Commissioner Doug Shulman.

Ernst joined the IRS last year after having been chairman and CEO of H&R Block from 1998 to 2007. He left Block to head the venture capital firm Bellevue Capital for two years before joining the IRS.

“Mark has been a most valued, respected and dedicated member of my leadership team, and he brought a unique perspective and focus to some of our most important initiatives, such as technology modernization, cybersecurity, financial management and workforce issues,” said Shulman. “I want to thank him for his strong contributions to the nation’s tax system, and he will be deeply missed by all of those who had the opportunity to work with him.”

Shulman noted that Ernst plans to return to the private sector. Succeeding him as deputy commissioner for operations support will be Beth Tucker, who currently serves as deputy commissioner for support in the IRS’s Wage & Income division.”

Incidentally, Mr. Ernst’s replacement at HR Block was none other than Richard Breeden. Canadians might be interested to know that this is the Richard Breeden of Conrad Black fame.

HR Block and U.S. citizens abroad

In March of 2012, we had a lively discussion about a page on the HR Block page suggesting that U.S. citizens abroad should enter Voluntary Disclosure (whatever that is supposed to mean). The consensus was that HR Block didn’t understand either the issue or how OVDP worked. (You might read this discussion before retaining HR Block.)

It is clear that

There's good money to be made in US tax compliance – HR Block seeks its fair share from #americansabroad http://t.co/wdmsHEO7eW

— U.S. Citizen Abroad (@USCitizenAbroad) June 5, 2013

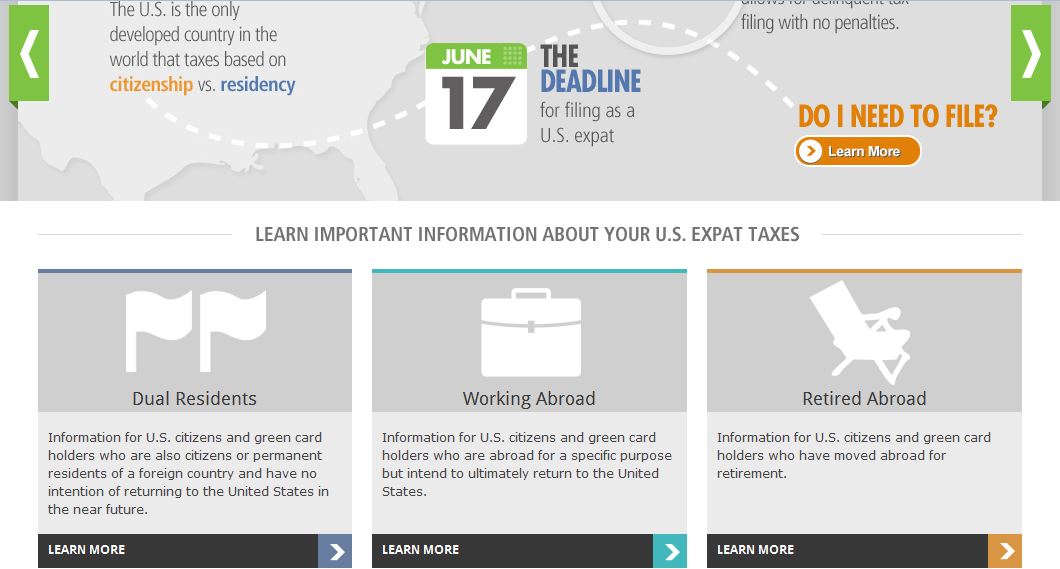

HR Block has clearly retooled itself (at least the marketing) so that U.S. citizens abroad “pay their fair share” to HR Block. Here is a snapshot of their opening page. Without reading the explanations, do you see a category that applies to “U.S. persons who are both working and living abroad indefinitely”?

The closest category is “Dual Residents”. Clearly U.S. citizens residing out of the United States indefinitely or “accidental Americans” living abroad are NOT “Dual Residents”.

Same soup warmed over – Do those people have any idea who their client base is?

Different kinds of tax preparers for #americansabroad – Make sure you know what you are dealing with http://t.co/Jk0Ymj1RRn

— U.S. Citizen Abroad (@USCitizenAbroad) June 5, 2013

Also, as a reminder. There are different categories of tax preparer. They include: lawyers, CPAs, EAs, and tax preparers. HR Block is in the last category. As Badger points out, the complexity of your situation dictates the kind of preparer you want.

Yes, time to enjoy yet again, the seemingly impossible task of getting knowledgeable yet ‘affordable’ US tax assistance from ‘abroad’ that falls somewhere between the likes of HR Block (not cheap either http://www.hrblock.ca/services/US_tax_pricing.asp ) and entering into an opaque and unlimited ‘terms of agreement’ – as even one local (and small) accounting firm insists on (while simultaneously refusing to provide even a gross estimate of the anticipated fee) – for preparing a mere puny 1040, reporting income barely large enough to meet the reporting threshold, plus the labyrinthine final forms for the pitiful registered Canadian “foreign trust” savings account closed in holy sacrifice – gone to pay professional fees to attain the practically impossible to achieve – but oh so blessed and esoteric state of US tax and reporting ‘compliance’ from ‘abroad’ and buy out involuntary servitude – and try to buy elusive peace of mind – with the usual zero US tax owed of course). As we know, we can’t afford to make even an inadvertent mistake no matter how small or non-existent the ‘US taxable’ income, or else it’s the US hangman and financial ruin for the likes of us living and working dual citizens outside the US.

I have a family member working at H&R block. They also sent an internal notice to their employees about the June deadline.

My God…who can be a good tax advisor to Americans Abroad. Who they can trust?

I wonder if H&R block is getting a portion of the funds collected via the IRS Whistleblower program?

http://www.irs.gov/uac/Whistleblower-Office-At-a-Glance

Good question, statelessman.

Thanks, USCitizenAbroad, for pointing out the difference between independent regulation and regulation tied to the IRS. Very troubling.

“Dual residency” is H & R Crock.

There is a little competition going on though. The IRS is actively training AARP members and retiree volunteers to give free tax help. This is seriously cutting in on H & R Block’s business.

May 30, 2013 11:05 ET

H&R Block Launches Remote Service, Augments In-Office Tax Prep for U.S. Citizens Living, Working Abroad

H&R Block Tax Experts to Help Expats Meet Deadline and Foreign Accounts Compliance

KANSAS CITY, MO–(Marketwired – May 30, 2013) – The United States is the only developed country that levies income taxes based on citizenship versus just residency. For the more than 6 million “expats” — Americans living abroad — the world’s largest tax preparation company launched a new remote service to help these taxpayers comply with their federal tax obligations. H&R Block (NYSE: HRB) is the only company that can serve this unique taxpayer in an office abroad or via a new remote service by their June 17 filing deadline.

H&R Block also launched a microsite for expats that answers many questions and outlines the filing responsibilities for those with dual citizenship and those who are working or retired abroad.

“Taxes can be confusing enough. Throw in the additional complexity of residing or working abroad and the simplest of tax situations can become more complicated,” said Kathy Pickering, executive director of The Tax Institute at H&R Block. “Whether the taxpayer has dual citizenship, works abroad or has retired to a tropical island paradise, H&R Block and its new microsite are here to help in-person and online.”

Expats can have their U.S. tax returns completed by H&R Block tax experts in an H&R Block office in more than 14 countries and U.S. territories. In addition, they can now work with a tax professional, using the company’s remote service. The remote service is a secure option that includes a customized interview to ensure an accurate return is prepared. Plus, all the benefits of an H&R Block office experience are available, including accuracy guarantees and the opportunity for free Second Look® reviews of past returns.

Know the filing requirements

U.S. citizens who meet the minimum income requirement — $19,500 for married filing jointly and $9,750 for single filers — are required to file a federal tax return regardless of where they live, even if all of their income was earned in a foreign country. Some taxpayers working abroad may be able to exclude some foreign income and claim a credit for foreign taxes paid on their U.S. tax return, which could offset any taxes owed to the United States.

Many expats also may have foreign bank or retirement accounts. The IRS recently announced it is working closely with United Kingdom and Australian officials to identify accounts held by Americans who may have a reporting requirement. The foreign bank account reporting form (FBAR) must be submitted to the Department of Treasury by June 30, but the information also may need to be included with the tax return on Form 8938, which is due earlier in the month.

“H&R Block’s expat tax experts have deep knowledge of the U.S. tax code in addition to the filing needs of this unique taxpayer,” said Kevin Mobley, director of international marketing at H&R Block. “We are bringing this expertise to the front door of every expat via our remote service.”

Taxpayers working abroad who are not able to file an accurate return by June 17 can submit a tax filing extension to make their filing deadline Oct. 15. While penalties are not assessed, interest accrues on any balance due from the April 15 filing deadline.

To find an international H&R Block office, visit expats.hrblock.com or call 800-HRBLOCK.