38 thoughts on “America can achieve goal of eliminating non-US bank services for Americans?”

It’s been clear to me for a long time that politicians (who should know better) and the general public (who can be excused for not knowing) view a foreign account as evidence for wrong doing. Why would anyone who lives in American or is an American citizen need a foreign account?

A large part of the American public can’t scratch together a couple of thousand if they have some kind of problem. So any kind of saving and investment is pretty limited.

Now I don’t think the politicians understand just how easy it is to put your money to work abroad without a foreign account. Americans can jack up the rates that corporations pay in the US and with a few mouse clicks and a few numbers for my limit orders I can sell IVV and purchase say VEU. Instantly I have escaped US corporate taxes. Jack up my individual taxes and it’s more important to me to escape the corporate ones as well.

A portion of my portfolio could be invested in the debts of American companies. Those companies borrowing the money could be growing. I get better after tax returns loaning my money to unproductive government programs since the interest is tax free. Want to build a football stadium, hospital or sewage treatment plant then no problem. I can led some money. An American company wanting to build a new building to house more workers is likely out of luck since the after tax returns are lower than the industries in bed with the government.

The problem isn’t the freezing U.S. bank accounts. They can freeze all of my U.S. bank accounts ( I don’t have any). The question is will they eventually be able touch my local bank accounts.

I think I will have to file and the ditch my American citizenship. This crap is never going to end. The homelanders will never change.

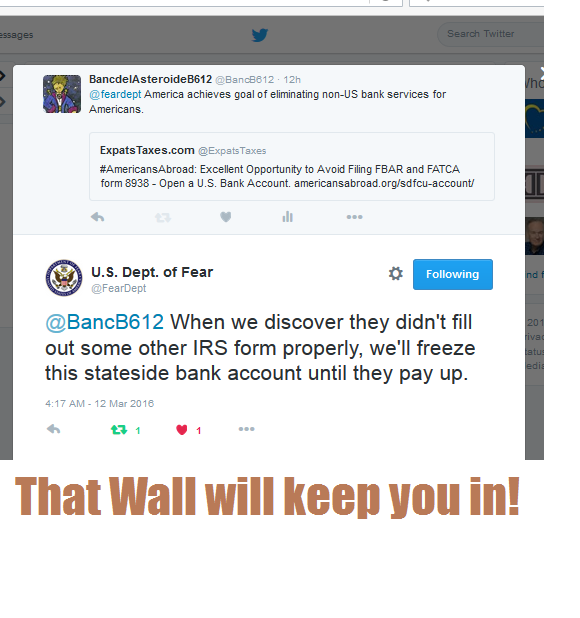

This bank service requires a $70 annual membership fee ($600 for lifetime) to American Citizens Abroad.

And hey presto – it’s now in ACA’s interest for the CBT/FATCA status quo to be maintained.

I guess the ACA don’t expect their Same Country Exception proposal to be adopted. So no conflict of interest.

Great observation, iota.

This is INSANE that I would be forced to bank in FOREIGN DOLLARS in a FOREIGN Country and do something that the country I live in actually considers offshore!!!

@George – also worth noting – being offshore, ACA bank customers escape FATCA but become subject to CRS reporting.

Bet they don’t put that in their brochure.

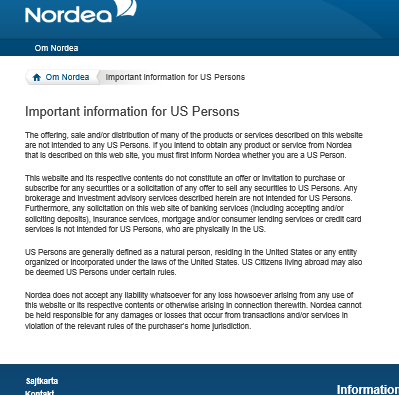

Nordea has a problem. Later this year every resident EU citizen will have the right to a basic bank account by EU directive.

I would suggest a resident EU citizen go into that bank (with a US place of birth) and remind the bank that it’s now the law they must provide a basic bank account.

Or forcing us to be Americans who happen to abide in other countries, George?

I find this “offer”, to open a bank account in a US government connected bank, the “State Department Federal Credit Union” so extremely repugnant and creepy, as do three of my U.S. contacts living in the UK. The U.S. really starts to resemble the former Soviet Union in more ways than one. Are people aware that during those dark years of the communist USSR, Soviet citizens living outside of the motherland had only one possibility to keep an account within the Soviet Union and that too was a special government bank account, also used by foreign Soviet diplomats and others? Now the U.S. makes this the only option for its unfortunate nationals who live outside of the U.S. prison. The intention? Your funds are well documented and under surveillance and should you ever do or say anything that you shouldn’t, or owe any tax, then you’ll never see your funds again. To imagine that American Citizens Abroad trumpet and promote this as if it was a welcome salvation. Why weren’t they capable of getting U.S. banks to respect the right of a U.S. citizen to have an account in the bank of their choice, in the country of their citizenship, even when the happen to live outside of the U.S. prison? Why was that so difficult to achieve? So, U.S. citizens have only one bank to choose from when living outside of the U.S. prison. Great. I’m sure their financial products and investment services and advisors are “highly competitive” and surpass all of the great world banks. OMG! It really is getting more and more Orwellian by the day. So lucky to have renounced and feeling a free human being again.

@iota, but the USA has not signed up to OECD CRS disclsoure.

Soooo ACA is encouraging by way of example, UK Residents to open offshore accounts;

To be brutally honest I DO consider offshore finances to be unethical and thats why its right to bank down the street!!!

OK, great. So, now how will people deal with receiving salary in countries where this has to be received into a LOCAL bank account?

@George – as I understand it (which I grant you is not a lot), the US has signed up to the original Convention but not (yet) the Protocol implementing automatic reciprocal exchange. And may never, since the CRS doesn’t have (or aspire to) FATCA’s power to extort the information under threat. In principle, though, the ACA account should eventually be subject to CRS reporting, which is a fact I think ACA should make clear in its advertising.

I agree with you that ACA is in danger of looking as if it’s encouraging non-US-resident US persons to open accounts for hiding money. That’s probably not their intention – naïveté and greed (for more members) seem more likely explanations. But if they’re really not in the market for dirty money, they ought to say so, or that’s what they’re likely to end up with.

But I don’t agree that there’s anything intrinsically unethical about an offshore account. It depends whether the account is or is not being used for illegal/unethical purposes. All non-US-resident US citizens need at least one offshore account: if their bank account isn’t offshore to one of their taxing authorities, it’s offshore to another.

For fifty years, without knowing it, I had offshore accounts. A few months ago I renounced, and since then haven’t had any.

As long as I have US retirement savings that will pay only into a US account, I must maintain an offshore account. There are legitimate reasons for having accounts in other countries. As long as tax is paid to the resident country, I have no problem with this. Here in Australia, our Prime Minister is quite open that he has investments in the Cayman Islands.

@Karen – I think the confusion is down to the fact that the US simply won’t accept that US citizens ever have a legitimate reason for having accounts in other countries, even if they live there.

As far as the US is concerned:

– a US account held by a US citizen who lives in Australia is not an offshore account,

– but an Australian account held by a US citizen who lives in Australia is an offshore account.

They’re wrong, but won’t admit it.

I think what some countries ought to do is withhold the same 30% that FATCA puts on banks that don’t follow the extraterritorial law, for payments TO U.S. banks from that country. If enough countries start redacting payments due to U.S. banks then we might see a change of heart from the U.S. government.

And that money withheld would go into a fund that helps pay for the costs of U.S. citizens residing in that country when it comes to tax/reporting preparation, penalties, cost for renouncing U.S. citizenship, etc. who couldn’t afford (or would have a hardship paying for) such on their own.

Barbadians feel the US has used its dominance to extort banking information while allowing Barbadian citizens to ‘stash’ money in the US undetected.

@Kelly

You’re assuming the US has a heart. But I agree, if the nation’s of the world organized themselves against FATCA, they could probably be successful at thwarting the US threat.

I wouldn’t count on the leader of the US’s largest trading partner doing this though, as he’s Barack’s new BFF.

American Citizens Abroad need to be applauded for making this credit union known to expats HOWEVER they are accepting credit and applause for something they have not done.

FACT;

1. State Department Credit Union has always accepted overseas applicants that are US Citizens!! This is NOT some special arrangement with American Citizens Abroad.

2. You do not need to join American Citizens Abroad and pay $60 a year to them to open an account because you could also join the American Consumer Council online for $5 but with promo voucher code CONSUMER it is f-r-e-e. After joinging ACC you then opt out of all the mailings.

3. Once you are a member of the credit union, you no longer need to meet the elegibility meaning you can quit what you joined with what was hopefully free.

4. If you become a member of the credit union, your family can become members because of you!!

What does George think? Our friends at ACA have been loosey goosey accepting congrats that they do not quite deserve..

@George

*To be brutally honest I DO consider offshore finances to be unethical and thats why its right to bank down the street!!!*

If it wasn’t for *offshore* in another country… my family who escaped a war… would have nothing… they ran with just the clothes on their backs & what they could carry… they didn’t plan to leave that way… but it was a choice of running or dying… some of our *offshore* is over 30 yrs old… passed down the generations that we added to… not alot… we are not talking multi-millions…. elders in my family do not trust the gov’t… the next generation also didn’t… my generation did trust the gov’t… look how that turned out for us… the elders were correct… never trust any gov’t…

@USFP, I do accept your premise.

Couple examples;

Is it appropriate for a Canadian Citizen resident in Canada to have a bank account in the USA absent extenuating conditions such as a florida condo? I say no.

Is it appropriate for an Irish Citizen resident in Ireland to have a a bank account in another EU country? Yes. the EU is a single bloc.

—————-

What I am getting at is that it is wrong/insane to be opening an account in the USA because of FATCA!!

Again I point out that the countries that don’t have any inter-governmental agreement (IGA) with the United States of America, and the non-FATCA banks therein, are listed on my website which is linked from all of my posts.

Simply open a bank in any of those countries and invest the funds locally. In many countries it is even possible to offer U.S. dollars accounts, as the central bank offers such accounts to local banks and is exempt from FATCA.

Now, you open a correspondent bank relationship with other banks in other countries (or their central banks, the way the Continuous Payment Settlement Bank in New York, N.Y., U.S.A. does) and now you have a multinational payment settlement system.

I would then offer reporting to I.R.S. if (a) the customer consents to it; (b) it makes the account FBAR exempt and therefore not part of the $10,000 threshold either; (c) the account number is redacted; (d) the bank sends the data to I.R.S. on a spreadsheet formatted to the bank’s convenience and I.R.S. parasites might need to write a program that reshuffles it to their convenience. Take it or leave it.

Folks – the angst is not worth it. Here is what FATCA and all of this means to almost every single expat who posts to or monitors this site: you will find your options limited should you move from wherever you live to somewhere else. Beyond that, not much.

Yes, that is wrong. It is, frankly, un-American. But it’s their country. They are entitled to exercise their sovereignty to damage it.

Canada – where most people on this site call home – has never asked where you were born to open a bank account until very recently. I certainly don’t advocate lying on forms even if some people here do. However if you have a defensible basis to deny US person-hood without having coughed up the $2350 to get the US government to bless you in that with a CLN, all you have to do is answer “no” to any form that asks you if you are a US person. You will never show up on any FATCA data exchange and you will never exist for the IRS or any of its minions.

That doesn’t make any of this right or fair. Any country that has a SIX MONTH waiting list to renounce membership at such a cost needs to give its head a shake. But that is their problem not yours.

Outside of Canada, it is a bit more nuanced since many countries DO routinely ask for place of birth and similar details when opening an account.

For 2nd generation expats, there is NOTHING to fear when they open that account since they are born abroad. Parents – “don’t let your daughters go up to be cowboys” may be a catchy song title, but “don’t let your children grow up to be Americans” is just plain common sense. If you left the USA after age 12 or 14 (I can’t recall what the cut-off is and don’t care!) and lived 10 years in the US, you have given your kids citizenship AIDS. Your sons will be subject to arrest for not registering for the draft and your daughters will be tax evaders. You don’t have to tell them and then they won’t have to lie. In the unlikely event they ever want to move there or you can actually afford tuition there, let them discover they can claim it then.

FATCA only requires counties to ask for a “reasonable” explanation as to why no CLN is available. For countries where this is an issue, I rather suspect that a $10,000 price tag for a family of four might just qualify. You have nothing to lose but your fear for trying. People in France or Switzerland should consider taking their govermments on since I think those countries actually ask where you are born.

If your government has signed on for FATCA and you have taken steps to become a non-US person, you don’t necessarily have to make the five years filing and eviscerate yourself for the IRS. Citizenship and taxation are not the same thing and citizenship is all that any government signed on for with FATCA. If you have become a citizen of another country and are prepared to say that you did so with the intent to lose your US ties, the USG has to acknowledge that under its own statutes, whether or not you have a CLN. You will never be “US tax compliant” but if you are not going to live their, you can add that to the list. I’m pretty sure you won’t be North Korean or Cuban tax compliant either. Comply with the laws of the country where you live – that takes enough mental energy for most.

Mobility is the real loss: a Canadian who wants to retire in the south of France will find those dreams harder to realize than the lottery if they happen to have been born in the US. For most, that dream is about as realistic as the winning lottery that will fund it.

All of this frightfully stupid and frightlfully wrong, but is not frightful. Everyone can take a nice deep breath and then let it out. By all means work for change, but please don’t add stress to your lives unnecessarily.

I think the difference between expat Americans and those from N. Korea and Cuba and others is this: they think they come from a place that is the light on the mountaintop. It isn’t. It’s just a country that occupies the middle of the North American landmass and seems to like guns. The latter trait is useful when you find your country invaded, but a nuisance the rest of the time. Relax.

One more thing: you can very likely visit the US as much you as you like. In fact, the more you do so with a non-US passport the better since you are building up a record of acting as a non-US person for State. You will, however, NEVER be able to live in that country again. That is the price to be paid for being born in the land of Liberty.

I remain astonished at the irony of it all – Cuba treats its expats better, believe it or not. I’m not sure about N. Korea.

As Steven Stills once wrote: if you can’t be with the one you love, well, love the one you’re with. Personally, that’s no problem. I do.

It’s been clear to me for a long time that politicians (who should know better) and the general public (who can be excused for not knowing) view a foreign account as evidence for wrong doing. Why would anyone who lives in American or is an American citizen need a foreign account?

A large part of the American public can’t scratch together a couple of thousand if they have some kind of problem. So any kind of saving and investment is pretty limited.

Now I don’t think the politicians understand just how easy it is to put your money to work abroad without a foreign account. Americans can jack up the rates that corporations pay in the US and with a few mouse clicks and a few numbers for my limit orders I can sell IVV and purchase say VEU. Instantly I have escaped US corporate taxes. Jack up my individual taxes and it’s more important to me to escape the corporate ones as well.

A portion of my portfolio could be invested in the debts of American companies. Those companies borrowing the money could be growing. I get better after tax returns loaning my money to unproductive government programs since the interest is tax free. Want to build a football stadium, hospital or sewage treatment plant then no problem. I can led some money. An American company wanting to build a new building to house more workers is likely out of luck since the after tax returns are lower than the industries in bed with the government.

The problem isn’t the freezing U.S. bank accounts. They can freeze all of my U.S. bank accounts ( I don’t have any). The question is will they eventually be able touch my local bank accounts.

I think I will have to file and the ditch my American citizenship. This crap is never going to end. The homelanders will never change.

This bank service requires a $70 annual membership fee ($600 for lifetime) to American Citizens Abroad.

And hey presto – it’s now in ACA’s interest for the CBT/FATCA status quo to be maintained.

I guess the ACA don’t expect their Same Country Exception proposal to be adopted. So no conflict of interest.

Great observation, iota.

This is INSANE that I would be forced to bank in FOREIGN DOLLARS in a FOREIGN Country and do something that the country I live in actually considers offshore!!!

@George – also worth noting – being offshore, ACA bank customers escape FATCA but become subject to CRS reporting.

Bet they don’t put that in their brochure.

Nordea has a problem. Later this year every resident EU citizen will have the right to a basic bank account by EU directive.

I would suggest a resident EU citizen go into that bank (with a US place of birth) and remind the bank that it’s now the law they must provide a basic bank account.

http://www.regulationtomorrow.com/eu/payment-accounts-directive-published-in-the-oj/

Or forcing us to be Americans who happen to abide in other countries, George?

I find this “offer”, to open a bank account in a US government connected bank, the “State Department Federal Credit Union” so extremely repugnant and creepy, as do three of my U.S. contacts living in the UK. The U.S. really starts to resemble the former Soviet Union in more ways than one. Are people aware that during those dark years of the communist USSR, Soviet citizens living outside of the motherland had only one possibility to keep an account within the Soviet Union and that too was a special government bank account, also used by foreign Soviet diplomats and others? Now the U.S. makes this the only option for its unfortunate nationals who live outside of the U.S. prison. The intention? Your funds are well documented and under surveillance and should you ever do or say anything that you shouldn’t, or owe any tax, then you’ll never see your funds again. To imagine that American Citizens Abroad trumpet and promote this as if it was a welcome salvation. Why weren’t they capable of getting U.S. banks to respect the right of a U.S. citizen to have an account in the bank of their choice, in the country of their citizenship, even when the happen to live outside of the U.S. prison? Why was that so difficult to achieve? So, U.S. citizens have only one bank to choose from when living outside of the U.S. prison. Great. I’m sure their financial products and investment services and advisors are “highly competitive” and surpass all of the great world banks. OMG! It really is getting more and more Orwellian by the day. So lucky to have renounced and feeling a free human being again.

@iota, but the USA has not signed up to OECD CRS disclsoure.

Soooo ACA is encouraging by way of example, UK Residents to open offshore accounts;

http://citywire.co.uk/new-model-adviser/news/hmrc-crackdown-uncovers-500000-uk-residents-offshore-accounts/a496880

To be brutally honest I DO consider offshore finances to be unethical and thats why its right to bank down the street!!!

OK, great. So, now how will people deal with receiving salary in countries where this has to be received into a LOCAL bank account?

@George – as I understand it (which I grant you is not a lot), the US has signed up to the original Convention but not (yet) the Protocol implementing automatic reciprocal exchange. And may never, since the CRS doesn’t have (or aspire to) FATCA’s power to extort the information under threat. In principle, though, the ACA account should eventually be subject to CRS reporting, which is a fact I think ACA should make clear in its advertising.

I agree with you that ACA is in danger of looking as if it’s encouraging non-US-resident US persons to open accounts for hiding money. That’s probably not their intention – naïveté and greed (for more members) seem more likely explanations. But if they’re really not in the market for dirty money, they ought to say so, or that’s what they’re likely to end up with.

But I don’t agree that there’s anything intrinsically unethical about an offshore account. It depends whether the account is or is not being used for illegal/unethical purposes. All non-US-resident US citizens need at least one offshore account: if their bank account isn’t offshore to one of their taxing authorities, it’s offshore to another.

For fifty years, without knowing it, I had offshore accounts. A few months ago I renounced, and since then haven’t had any.

As long as I have US retirement savings that will pay only into a US account, I must maintain an offshore account. There are legitimate reasons for having accounts in other countries. As long as tax is paid to the resident country, I have no problem with this. Here in Australia, our Prime Minister is quite open that he has investments in the Cayman Islands.

@Karen – I think the confusion is down to the fact that the US simply won’t accept that US citizens ever have a legitimate reason for having accounts in other countries, even if they live there.

As far as the US is concerned:

– a US account held by a US citizen who lives in Australia is not an offshore account,

– but an Australian account held by a US citizen who lives in Australia is an offshore account.

They’re wrong, but won’t admit it.

I think what some countries ought to do is withhold the same 30% that FATCA puts on banks that don’t follow the extraterritorial law, for payments TO U.S. banks from that country. If enough countries start redacting payments due to U.S. banks then we might see a change of heart from the U.S. government.

And that money withheld would go into a fund that helps pay for the costs of U.S. citizens residing in that country when it comes to tax/reporting preparation, penalties, cost for renouncing U.S. citizenship, etc. who couldn’t afford (or would have a hardship paying for) such on their own.

http://www.nationnews.com/nationnews/news/78644/-lopsided-fatca

Barbadians feel the US has used its dominance to extort banking information while allowing Barbadian citizens to ‘stash’ money in the US undetected.

@Kelly

You’re assuming the US has a heart. But I agree, if the nation’s of the world organized themselves against FATCA, they could probably be successful at thwarting the US threat.

I wouldn’t count on the leader of the US’s largest trading partner doing this though, as he’s Barack’s new BFF.

American Citizens Abroad need to be applauded for making this credit union known to expats HOWEVER they are accepting credit and applause for something they have not done.

FACT;

1. State Department Credit Union has always accepted overseas applicants that are US Citizens!! This is NOT some special arrangement with American Citizens Abroad.

2. You do not need to join American Citizens Abroad and pay $60 a year to them to open an account because you could also join the American Consumer Council online for $5 but with promo voucher code CONSUMER it is f-r-e-e. After joinging ACC you then opt out of all the mailings.

3. Once you are a member of the credit union, you no longer need to meet the elegibility meaning you can quit what you joined with what was hopefully free.

4. If you become a member of the credit union, your family can become members because of you!!

What does George think? Our friends at ACA have been loosey goosey accepting congrats that they do not quite deserve..

@George

*To be brutally honest I DO consider offshore finances to be unethical and thats why its right to bank down the street!!!*

If it wasn’t for *offshore* in another country… my family who escaped a war… would have nothing… they ran with just the clothes on their backs & what they could carry… they didn’t plan to leave that way… but it was a choice of running or dying… some of our *offshore* is over 30 yrs old… passed down the generations that we added to… not alot… we are not talking multi-millions…. elders in my family do not trust the gov’t… the next generation also didn’t… my generation did trust the gov’t… look how that turned out for us… the elders were correct… never trust any gov’t…

@USFP, I do accept your premise.

Couple examples;

Is it appropriate for a Canadian Citizen resident in Canada to have a bank account in the USA absent extenuating conditions such as a florida condo? I say no.

Is it appropriate for an Irish Citizen resident in Ireland to have a a bank account in another EU country? Yes. the EU is a single bloc.

—————-

What I am getting at is that it is wrong/insane to be opening an account in the USA because of FATCA!!

Again I point out that the countries that don’t have any inter-governmental agreement (IGA) with the United States of America, and the non-FATCA banks therein, are listed on my website which is linked from all of my posts.

Simply open a bank in any of those countries and invest the funds locally. In many countries it is even possible to offer U.S. dollars accounts, as the central bank offers such accounts to local banks and is exempt from FATCA.

Now, you open a correspondent bank relationship with other banks in other countries (or their central banks, the way the Continuous Payment Settlement Bank in New York, N.Y., U.S.A. does) and now you have a multinational payment settlement system.

I would then offer reporting to I.R.S. if (a) the customer consents to it; (b) it makes the account FBAR exempt and therefore not part of the $10,000 threshold either; (c) the account number is redacted; (d) the bank sends the data to I.R.S. on a spreadsheet formatted to the bank’s convenience and I.R.S. parasites might need to write a program that reshuffles it to their convenience. Take it or leave it.

Folks – the angst is not worth it. Here is what FATCA and all of this means to almost every single expat who posts to or monitors this site: you will find your options limited should you move from wherever you live to somewhere else. Beyond that, not much.

Yes, that is wrong. It is, frankly, un-American. But it’s their country. They are entitled to exercise their sovereignty to damage it.

Canada – where most people on this site call home – has never asked where you were born to open a bank account until very recently. I certainly don’t advocate lying on forms even if some people here do. However if you have a defensible basis to deny US person-hood without having coughed up the $2350 to get the US government to bless you in that with a CLN, all you have to do is answer “no” to any form that asks you if you are a US person. You will never show up on any FATCA data exchange and you will never exist for the IRS or any of its minions.

That doesn’t make any of this right or fair. Any country that has a SIX MONTH waiting list to renounce membership at such a cost needs to give its head a shake. But that is their problem not yours.

Outside of Canada, it is a bit more nuanced since many countries DO routinely ask for place of birth and similar details when opening an account.

For 2nd generation expats, there is NOTHING to fear when they open that account since they are born abroad. Parents – “don’t let your daughters go up to be cowboys” may be a catchy song title, but “don’t let your children grow up to be Americans” is just plain common sense. If you left the USA after age 12 or 14 (I can’t recall what the cut-off is and don’t care!) and lived 10 years in the US, you have given your kids citizenship AIDS. Your sons will be subject to arrest for not registering for the draft and your daughters will be tax evaders. You don’t have to tell them and then they won’t have to lie. In the unlikely event they ever want to move there or you can actually afford tuition there, let them discover they can claim it then.

FATCA only requires counties to ask for a “reasonable” explanation as to why no CLN is available. For countries where this is an issue, I rather suspect that a $10,000 price tag for a family of four might just qualify. You have nothing to lose but your fear for trying. People in France or Switzerland should consider taking their govermments on since I think those countries actually ask where you are born.

If your government has signed on for FATCA and you have taken steps to become a non-US person, you don’t necessarily have to make the five years filing and eviscerate yourself for the IRS. Citizenship and taxation are not the same thing and citizenship is all that any government signed on for with FATCA. If you have become a citizen of another country and are prepared to say that you did so with the intent to lose your US ties, the USG has to acknowledge that under its own statutes, whether or not you have a CLN. You will never be “US tax compliant” but if you are not going to live their, you can add that to the list. I’m pretty sure you won’t be North Korean or Cuban tax compliant either. Comply with the laws of the country where you live – that takes enough mental energy for most.

Mobility is the real loss: a Canadian who wants to retire in the south of France will find those dreams harder to realize than the lottery if they happen to have been born in the US. For most, that dream is about as realistic as the winning lottery that will fund it.

All of this frightfully stupid and frightlfully wrong, but is not frightful. Everyone can take a nice deep breath and then let it out. By all means work for change, but please don’t add stress to your lives unnecessarily.

I think the difference between expat Americans and those from N. Korea and Cuba and others is this: they think they come from a place that is the light on the mountaintop. It isn’t. It’s just a country that occupies the middle of the North American landmass and seems to like guns. The latter trait is useful when you find your country invaded, but a nuisance the rest of the time. Relax.

One more thing: you can very likely visit the US as much you as you like. In fact, the more you do so with a non-US passport the better since you are building up a record of acting as a non-US person for State. You will, however, NEVER be able to live in that country again. That is the price to be paid for being born in the land of Liberty.

I remain astonished at the irony of it all – Cuba treats its expats better, believe it or not. I’m not sure about N. Korea.

As Steven Stills once wrote: if you can’t be with the one you love, well, love the one you’re with. Personally, that’s no problem. I do.

That’s the reality of it.