UPDATE January 24, 2015: THIRD OF FIVE LEGAL BILLS PAID

[We now have a NEW POST taking us up to May 1, 2015. This post will be retired from service.]

On August 11, 2014, Constitutional Litigator Joseph Arvay filed a FATCA IGA lawsuit in Canada Federal Court on behalf of Plaintiffs Ginny and Gwen, the Alliance for the Defence of Canadian Sovereignty (en français), and all peoples worldwide. Read Alliance’s Claims and comment on our Alliance blog.

Chers amis et donateurs,

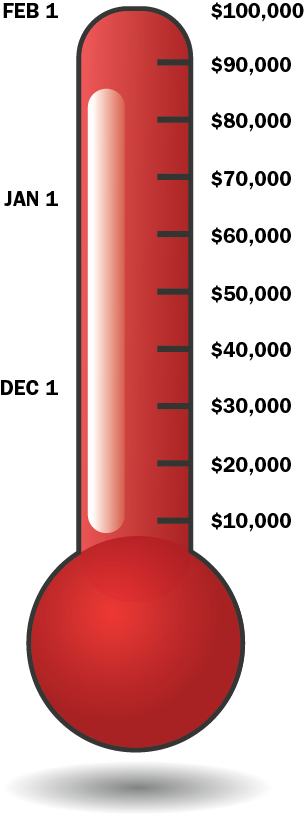

Ensemble, nous avons atteint notre but : ramasser les fonds nécessaires pour payer la troisième des cinq factures légales de notre poursuite judiciaire.

Ramasser 300 000 $ provenant de petits dons est un exploit tout à fait extraordinaire et nous invitons notre gouvernement canadien, ainsi que tous les autres gouvernements qui ont piétiné les droits de leurs citoyens, à en prendre bonne note.

Chaque jour, nous nous rapprochons de notre but. Déjà, nous avons ramassé plus de la moitié des fonds nécessaires pour payer les frais légaux de notre poursuite contre le gouvernement canadien et l’entente FATCA.

Si nous avons parcouru un si grand bout de chemin, c’est grâce à nos deux courageuses plaignantes, Ginny et Gwen, à nos donateurs provenant du Canada et de partout dans le monde, ainsi qu’aux administrateurs des sites Internet Isaac Brock Society et Maple Sandbox. Ils permettent tous à nos voix d’être entendues.

Merci !

L’équipe de l’ADSC

———————————————————————————————–

Dear Friends and Supporters,

Together we have reached our goal of paying off the third of five retainer fees for our Canadian FATCA IGA lawsuit.

Raising $300,000 from small donations is a pretty amazing achievement and we ask the Government of Canada, and those other governments who have also tossed away rights of their citizens, to take notice.

It’s still a marathon, but we are more than half way to pay off the Federal Court legal costs.

We have come so far because of our brave Plaintiffs, Ginny and Gwen, our Canadian and International donor-supporters, and the administrators of the Isaac Brock and Maple Sandbox websites who make it possible for our voices to be heard.

Thank you all,

—The ADCS-ADSC team

@StephenKish – a few more musings that may be of some assistance to the legal team preparing the case. I tried to post this on the ACDSovereignty blog, but it appears not to have gone through (the page just froze when i tried to post it). This is really written for the possible use of the Arvay team – I THINK I’m done venting and since I have the training, I couldn’t resist using it a bit. I hope they can find something useful in all of this. For our non-legal browsers, forgive me if I have delved to often into legal terminology below but I hope this will help gel some of the arguments in your minds as well. Pardon me in advance for the length! Here goes (and thanks to @George for directing me to the Convention – a useful additional bit of data for me):

Canada is a signatory to the 1930 Hague Convention regarding nationality. While the US is not a signatory (it was done under the auspices of the League of Nations which the US did not join), the US did in fact amend their citizenship laws in significant measure to conform to the Convention. Several provisions of the Convention are relevant here:

Article 1

It is for each State to determine under its own law who are its nationals. This law shall

be recognised by other States in so far as it is consistent with international

conventions, international custom, and the principles of law generally recognised with

regard to nationality.

Article 2

Any question as to whether a person possesses the nationality of a particular State

shall be determined in accordance with the law of that State.

Article 3

Subject to the provisions of the present Convention, a person having two or more

nationalities may be regarded as its national by each of the States whose nationality he

possesses.

…

Article 5

Within a third State, a person having more than one nationality shall be treated as if

he had only one. Without prejudice to the application of its law in matters of personal

status and of any conventions in force, a third State shall, of the nationalities which

any such person possesses, recognise exclusively in its territory either the nationality

of the country in which he is habitually and principally resident, or the nationality of

the country with which in the circumstances he appears to be in fact most closely

connected.

The combination of these Articles of the Hague Convention on Nationality (esp. Art. 3 & Art. 5) is the essence of the “Master Nationality Rule” under international law. Each State is competent to make its own laws regarding nationality which others shall recognize (proviso in Art. 1 though that they be in accordance with customary international law in that regard – not relevant to us here).

In relation to FATCA and C-31 we need to take note of Art 3 (dual nationals to be regarded as nationals of the state where they are) and Art 5 (closest connection test to determine which nationality is dominant in the case of 3rd states).

With FATCA, the US has effectively told the world that it chooses to ignore Art 3 and seeks to have, among others Canada, recognize its claim to impose US citizenship on potential nationals beyond its borders who are not themselves claiming the privilege. This is an astonishing claim. The Convention would recognize that the US can impose such citizenship (and tax) laws as it chooses within its own borders. However, by asking Canada to recognize those laws in relation to Canadian nationals resident in Canada, the US is effectively stepping outside the bounds of customary international law (as recognized by this treaty) to which Canada is bound. Reference to International Law in relation to identifying and enforcing Charter rights is certainly not unheard of. It is certainly relevant to a s. 1 justification claim.

Note as well that the Canada:US Tax Treaty – at least as it stood prior to C-31 – specifically carved out of Canada’s obligations any obligation to provide the US assistance in relation to tax claims against US citizens from and after the date they become Canadians. As I have pointed out elsewhere, Neither C-31 nor the IGA it enforces have purported to amend the US Canada Tax Treaty and could not do so since the IGA does not have force of treaty in the US. The IGA was merely created by way of an “executive order” to by-pass the Senate and the requirements of the US Constitution for treaties to be ratified by the Senate. It has the internal status in the US akin to an interpretation bulletin here: something they intend to act upon but are in no ways bound to do so.

In considering the defence that C-31 is “saved” by s. 1 of the Charter, the fact that it is out of step with Canada’s international undertakings, that it is responding to threats made (via FATCA) to Canada’s economic interests which themselves were violations of international law and the US Canada Tax Treaty (and the IGA is NOT a US Treaty, to repeat!) will be relevant arguments.

I would also add a note regarding the question of “damages” suffered by US Persons targeted by C-31. Canada’s tax treaty (and pronouncements made in Parliament by the Minister) make it clear that Canada is NOT helping to collect US taxes, still less fines and penalties, from Canadian citizens. The OBJECT of C-31 is to facilitate the US in making demands of them even if it won’t help enforce or collect by the automatic, warrant-less exchange of information. We need to make it quite clear to the un-informed exactly how burdensome this can be. A Canadian who is involuntarily identified in Canada by Canada as a US Person despite their Canadian citizenship must now live permanently under the following handicaps if, having been forcibly “outed” against their will, they CHOOSE to “become compliant” with US law while living in Canada:

1. He or she will be unable to enter into business with other Canadians through partnerships, small business corporations or unincorporated associations unless all of his or her Canadian partners consent to the requirement for detailed and confidential data regarding all financial accounts of that business to be made available electronically to the IRS in a foreign country.

2. He or she will be unable to be practice as a partner in a professional law or accounting firm unless the firm permits the disclosure of all of its financial accounts to the IRS in a foreign country and unless any professional bodies governing such firm (Law Society, CICA, etc.) permit the release of client-specific trust account information to the IRS in a foreign country.

3. He or she will be unable to accept employment involving managing bank accounts for an employer unless the employer consents to the release of detailed records of its financial accounts and ownership to the IRS in a foreign country.

4. He or she will be prohibited from owning most mutual funds offered for sale in Canada (as these do not provide the reporting needed for “PFIC” reports to the IRS) while Canadian securities laws will prohibit the purchase of US compliant mutual funds.

5. He or she may be denied access to some company pension plans if they are not recognized by the IRS and may be denied the benefits of various tax incentive programs enacted by Parliament with the intention of encouraging Canadians to engage in socially useful behaviour (including saving for retirement, saving for disability, TFSA’s or saving for education). He or she will be denied access (in part) to incentives to encourage home ownership and will thus be less able than other Canadians to aspire to or undertake that step.

6. He or she may be compelled to register for possible military service (Selective Service or the Draft) under potential criminal penalties for failure to comply.

7. All data transmitted to the IRS will be done so electronically, will be subject to risk of hacking, will be available for use by other US agencies for unknown purposes and any recourse regarding misuse of such data would be solely before foreign courts or tribunals

The foregoing are just a few of the foreseeable consequences of C-31. Remember – NO foreign law, including US law, applies in Canada. Canadians targeted either by the long-arm provisions of the US Tax Code or FBAR/FINCEN requirements have every right, as Canadians, to decline to submit to the jurisdiction of US law or courts while living in Canada. Their right to do so is all the more evident where the US exercise of long arm jurisdiction is unique and in some aspects contrary to customary international law. While not requiring ANY Canadian to actually comply with US law while living in Canada, C-31 seeks to identify potential US Persons to US enforcement agencies. The only foreseeable consequence of this of course is that the US Persons so identified will become compliant or they will not. There is hardly any purpose in identifying US Persons who have not been compliant so that they can choose not to be compliant. The only rational view of C-31 is that it was intended to COMPEL all US Persons in Canada to become compliant with US law while living in Canada, regardless of their prior choice. The form of compulsion chosen is the threat of the disclosure of private, personal data to a foreign government by Canada – in other words, being “outed”. If the victims of such coercion choose to become compliant, the consequences listed above are absolutely foreseeable consequences. Canada is correct that it is US law the creates the harm, but it is Canadian law (C-31) which makes otherwise ineffective or toothless US law in Canada effective. Canada cannot help the US aim the gun, identify the victim and then deny any responsibility for the obvious and intended outcome.

A simple analogy makes the point. Requiring gay people to be identified and then automatically sharing that information with a party who, armed with the information, can harm them is not a neutral action any more than sending a register of black people living in Canada to the KKK is a neutral action. A party intends the ordinary and foreseeable consequence of their actions and Canada, by disclosing the identity and private financial affairs of potential US Persons to a foreign government must accept the consequences of that action. The consequence – described above – is the subjection of the persons so identified to perpetual handicap while living in Canada. Those foreseeable – indeed, intended – consequences of disclosure cannot be divorced from the act of disclosure when considering the Constitutional validity of the law which made the disclosure.

Prior to C-31, we know that few, if any, potential US Persons living in Canada were in fact “compliant”. The number of returns filed in the US from Canada is trivial compared to the hundreds of thousands, if not millions, of potential US Persons living here. This is not, however, a numbers game. The Charter arguments would be the same if FATCA and C-31 only sought to uncover a single Canadian, after all. The ONLY point of FATCA is to seek information the US did not already have about US Persons it could not otherwise identify. With C-31, Canada has agreed to out any Canadians who MIGHT fit the bill. No other nationality is singled out for this treatment – Canadian citizens of Chinese, North Korean or Cuban origin do not live in fear that their private personal data will be automatically transmitted to a land they or their parents may have fled from.

What then of the Canadian who, though “outed” , chooses not to comply?

1. They may find themselves on the receiving end of US enforcement proceedings which may include threats of arrest or imprisonment as well as financial demands which are designed to be in terrorem and would amount to the virtual confiscation of the life savings of any victim of such demands by reason of the multiplication of FBAR penalties alone.

2. Were warrants for arrest to be issued in consequence of Canada’s action, the object of such warrants could be subject to forcible rendition into the US should they take a domestic Canadian flight should the pilot decide (unknown to the passengers) to take a flight route involving transit over US airspace to conserve fuel. Canadian planes do this hundreds of times per day and each such flight is subject to being forced to land in the US should the US so decide.

Prior to FATCA, few US Persons had the tiniest inkling of the magnitude of the handicaps the US intends to impose upon those of its citizens or former immigrants who reside abroad. Few can learn of the full breadth of such vicious, narrow-minded laws without being offended to the core of their being. Clearly the US is either ignorant of the circumstances of those upon whom they bestow the blessings of citizenship abroad or they do not care. No country on earth subjects its people to that treatment and the only conclusion possible is that the US considers it a form of treason to live outside of it. Those few that were aware, or have become aware and wish to have nothing to do with them, formerly had the protection of their own country (Canada) plus the knowledge that the US lacked any means to enforce these measures beyond their borders. C-31 has chosen to single them out though and deprive them of their choice not to comply.

As noted, the only possible object of C-31 is to compel those who are not compliant with US law in Canada to become compliant. Becoming compliant with US law while living a normal, middle-class life in Canada involves tremendous hardship and limitation of career options as noted above. C-31 – by choosing to single out US Persons from among all other “hyphenated” Canadians – uniquely singles them out for this handicapped existence and deprives them of the choice to ignore the US while living in Canada.

There is of course a third option. Renounce (or its cousin, Relinquish). Two thoughts need to be borne in mind here. Firstly, the US has been throwing roadblocks and obstacles in front of this path for the past 25 years or so. Space prevents me from listing all the laws passed since 1994 imposing ten year tax filing obligations, exit taxes, renunciation fees added in 2011 then quintupled in 2014, lengthy waiting lists, etc. The party choosing to undertake this path must first VOLUNTARILY disclose their existence to the US. Thus, C-31 coercing Canadians into renunciation by threatening to disclose their private financial and other data to the US cannot escape the consequences of that action by arguing that the victims can renounce when the consequence of doing so is disclosure of all of that same data plus all the handicaps described above. The only improvement renunciation offers is a foreseeable end to the pain in future years (and at a steep price). Amnesty programs are all flawed and, in any event, fully discretionary. These can hardly be pointed to as mitigation of the effects of C-31.

Secondly, recall the Treaty provisions above. US law determines who is a US Person and, despite what many may think, that is in fact the correct position. Canada can’t decide US citizenship law for the US. Normally, that does not matter since, under the Treaty, we have no obligation to give effect to foreign nationality rules inside our borders in relation to our own nationals. A further adverse impact of “outing” under C-31 is that it subjects the INNOCENT (i.e. an “undocumented” non-US Person) to the peril of having to prove their non-status in a US proceeding. Needless to say, that is a foreign proceeding before a foreign tribunal and with no recourse to Canadian courts. A Canadian who certifies that they are NOT a US Person but does not possess a CLN may be compelled to obtain one in order to prevent their data from being transmitted. Applying for a CLN, of course, involves transmission of some or all of that same data (since compliance to the effective date of the CLN is a requirement). Not all Canadians live in a city where the US has a Consulate or Embassy, so getting a CLN involves a commitment of time and money. As well, should the US contest the entitlement to a CLN, there is no recourse in Canada. The only option is to submit to US courts and US process to try to establish, in the US, that one is not one of them. No Canadian is obliged to establish their loss of prior nationality to enjoy all the benefits of Canadian citizenship save and except US-born Canadians.

The arguments discussed above of course apply with still more force in the case of Canadian born US Persons who owe their unfortunate status to a Green Card not surrendered in the prescribed fashion for tax purposes or to having been born in Canada to US-born parents.

Hope some of this is useful to the team and informative to some of our lay readers.

.

@Anne Frank: Wow! Thanks!

Anne Frank,

Again, I am (especially as parent of a Canadian-born US-defined US citizen adult son without ‘requisite mental capacity’ for whom renunciation is impossible FOR ANY AMOUNT OF $$$ SPENT) / we are indebted for your analysis of all of this. Very informative and I am sure will be so useful to the litigation team. I’ll say it again — what would we do without the legal minds and all the other expertise we find here?.

Because I’m on a bit of a tear (hopefully not a rant), I thought I’d expand a bit on the concept of enforcing foreign law in Canada and the concept of forcing Canadians to prove the negative fact (“I am not a US Person”) through proceedings in a foreign country.

Let’s start with foreign law. There are all kinds of laws that countries devise that impose obligations on their nationals. In some cases, these laws have no application beyond their borders and don’t purport to. In others, they have no explicit limit. Canada imposes tax on your worldwide income, if you are resident. Standing one foot outside the border on New Year’s Eve won’t change that. Even moving abroad for a year with no intention to sever links will change it. Let’s look at some other types of laws:

• Conscription: while we don’t normally prevent Canadian citizens who hold a second passport from fulfilling their military service obligations to other countries whose nationality they may hold (although that is not true if it involves Somalia, Syria or other hot spots), we certainly don’t enforce those laws either. Can anyone seriously expect a Canadian law requiring Chinese, North Korean, Cuban, Russian, Swiss, Israeli, etc. citizens resident in Canada to disclose their age, address and nationality to their “other” nationality to survive a Charter challenge? The proposition is intended to sound absurd. It would be an outrageous intrusion into their privacy, discrimination based on national origin, etc. There is nothing in principle to distinguish such laws from the US fiscal laws that C-31 has allowed Canada to become an auxiliary enforcement agent of.

• Taxation : the point has been made before but bears repeating. Canada does not assist Eritrea in identifying Eritrean Canadians to whom Eritrea may wish to send demands for the filing of benign (by comparison to the US regime) CBT tax forms. To the contrary, Canada protests the mere existence of the tax and expels Eritrean diplomats who even mention the matter on unsolicited phone calls to their Embassy. What if ISIS took over in Iraq and started demanding Canada provide data regarding Christian and Yazidi refugees in Canada so it could seek to collect the dimmi tax from non-Muslim citizens? These examples readily put paid to the proposition that delivery of information necessary to the enforcement of foreign tax and citizenship laws in Canada upon Canadians is a neutral act that can be examined under the Charter independent of the intended, foreseeable consequences of the information sharing.

• Religion: this is not a big stretch. There are many countries in the world for whom apostasy is a capital crime. Should Canada start to provide data regarding dual-citizen converts from Islam within Canada so that our citizens should be in danger of a complimentary beheading on their next visit to the old country to visit their grandmother?

One could continue down this line all day. The examples are extreme and the answers are obvious yet there is no obvious or principled distinction between those examples and C-31 beyond the fact that Canada hasn’t (yet) chosen to do it.

The assistance we provide foreign governments for the enforcement of their laws (eg. Extradition, tax treaty information exchanges) is invariably connected to activities of individuals OUTSIDE of Canada and conditioned by some level of reciprocity. There can be no reciprocity for CBT since no other country practices it. Extradition for a crime committed by a Canadian outside of Canada (subject to safeguards, of course) is subject to, among other things, an examination of whether Canada would also consider the action to be a crime (CBT would not pass that exam). Outside of the tiny number of cases of internationally recognized instances of universal criminal jurisdiction (crimes against humanity, for example, sex tourism being an emerging one) I can think of no precedent whatsoever for ANY country assisting in the enforcement of foreign laws regarding actions on their own soil against their own nationals (including those who happen to have dual citizenship). If, pre-FATCA, there is a single example of this, I have not discovered it (I have not considered and don’t think relevant any reciprocal enforcement rules within the EEC which is a supra-national hybrid entity).

No other Canadian has to prove they are not hyphenated. Chinese Canadians don’t have to prove they have lost Chinese citizenship because we don’t enforce Chinese law over them. We don’t need to know or care about Chinese laws of citizenship or loss of citizenship as regards a former Chinese national who has validly acquired Canadian nationality. In that context, it matters not how fair or onerous, vindictive or lax Chinese law may be. While the 1930 Hague Convention on Nationality defers to each country to set its own rules regarding nationality, it obliges no state to have regard to those rules as regards (i) its OWN nationals; or (ii) dual citizens whose residence or closest connection is elsewhere. In those circumstances, nationality is something CLAIMED by an individual, not forced upon them. With CBT and FATCA, the US has turned nationality into a millstone. Asking for assistance in the enforcement of uniquely punitive citizenship laws is beyond anything contemplated by international law. US law creates a reverse onus – the onus of the Canadian seeking to demonstrate loss of US Person status at an earlier date is on them. When Canada requires a CLN to demonstrate non-US Person status and avoid loss of privacy, it requires that they surrender their privacy (by seeking a CLN) in order to preserve it. I hope that makes the argument a bit clearer.

OK, now I’m REALLY done!

Anne Frank,

I had this in a comment some time ago:

George had pointed out to me that my son was born in Canada well prior to the date of “Denunciation” — how does “denunciation” work / the shredding of all signed in 1930?

@EmBee

Well that’s allright, you couldn’t guess that I have been living in France since 1975.

Now, there’s something very interesting over here in France that shows it’s democray is ahead of most other democracies in the world. And that is the fact tha the french have 12 legal representitives abroad. I contacted parlement deputy Frederic Lefebvre who legally represents the french citizens living in north america. I’ve been exchanging mails with him. He has spoken up against the FACTCA IGA agreement signed by the socialist gouvernment here in November 2013 in parlement several times to defend french citizens who also have american nationality or are green card holders that are now living in France and are affected by FATCA. I’ve been feeding him with all the legitat information I can about how illegal and desriminatory this all is.

I think you should contact him and associate your fight in Canada with his here in France.

Here are a few links :

Most important : http://www.frederic-lefebvre.org/fatca/ THIS IS GETTING BIG OVER HERE

http://www.frederic-lefebvre.org/facta-reminder-of-the-social-role-of-french-banks-the-huffington-post/

http://www.frederic-lefebvre.org/fatca-frederic-lefebvre-defend-motion-dajournement-du-projet-dapprobation/

Did you know that the mayor of London, born in New York is outraged by FATCA. He says he’ll never ever file in a 1040, the IRS can go fly a kite on Mars.

Read latest article about Boris Johnson : http://www.forbes.com/sites/robertwood/2014/11/18/mayor-boris-johnsons-terrible-horrible-no-good-very-bad-day-as-an-american/

I’m going to send a mail to him and to frederic Lefebvre to propose us to gather all together here in Europe to do what you are doing in Canada

The whole world is raising fists now at the american empire and taking act.

Looks like the Obama administration shot a bullit in it’s foot with FATCA.

Keep in touch between Europe and Canada

@AnneFrank, I have long said the core problem is this is a citizenship issue not a tax issue.

Again Article 1 of the 1930 Convention;

—

Article 1

It is for each State to determine under its own law who are its nationals. This law shall be recognised by other States in so far as it is consistent with international conventions, international custom, and the principles of law generally recognised with regard to nationality.

—

When the United States states that a Canadian Citizen resident/present in Canada is a United States Citizen they are effectively nullifying all Canadian Citizenship laws.

I am most familiar with the laws of the UK and the Republic of Ireland. I would suspect that similar language could be found in Canada because of the shared heritage.

In the UK and the ROI you are either a British Citizen, a UK Citizen, a Commonwealth Citizen, an Irish Citizen or most importantly you are an Alien.

The laws of the UK and ROI define the above and solely the above. They do NOT define US Citizen and in fact a US Citizen not being one of the above can solely be an ALIEN.

Key section of the British Nationality Act;

” alien ” means a person who is neither a Commonwealth citizen nor a British protected person nor a citizen of the Republic of Ireland”

Key Section of the ROI Aliens Act;

“Every person who is a citizen of the United Kingdom of Great Britain and Northern Ireland is hereby exempted from the application of the

provisions of the Aliens Act, 1935 (No. 14 of 1935) , and from the application of the provisions of every aliens order made under section 5 of that Act before the making of this order.”

——-

The United States does the same thing, you are either a USC or an Alien.

Where am I going with this? Whilst these countries might tolerate the current term called “dual nationality” they do NOT recognize this common phrase in law!!

British Citizenship in the UK trumps any other countries laws simply because no other status is recognized! Slight step back…under the Treaty of Rome (EU) the additional citizenship of EU Citizenship is recognized.

In regards to Canada, can the two plaintiffs be anything other than Canadian Citizens under the law of Canada? I have to say NO.

@Calgary411, “George had pointed out to me that my son was born in Canada well prior to the date of “Denunciation” — how does “denunciation” work / the shredding of all signed in 1930?”

Let me have a go at this though far better minds than my own will do better.

Pre-denunciation is a slam dunk IMO as per your son.

Post that date, we have to ask does Canada recognize in principle the master nationality rule. In one of the 7 FAMS even the USA does!!

Beyond that you have to ask does the law of Canada recognize in any manner the imposed citizenship by a foreign government on an existing Canadian Citizen?

Let me speak in regards to the Republic of Ireland.

Under Irish Law, they recognize Irish Citizenship, British Citizenship, EU Citizenship. All else are ALIENS.

In regards to the UK, they recognize Irish Citizenship, Commonwealth Citizenship, British Citizenship. All else are ALIENS.

I suspect Canada has similar law, you are either a Canadian Citizen or an ALIEN.

If you are an Irish Citizen it is impossible to be a Alien at the same time meaning you can not also be a US Citizen because that is an Alien.

But…..Irish Law would allow you to also be a British Citizen or an EU Citizen at the same time!

In the back of my mind, I remain convinced that US Citizens living elsewhere in the world are in fact screwed. The US is their sole and only master and they are guests in the country they live in.

@anne frank and geroge thank you so much for the above read. very interesting.

mr. harper and mr. obama……take that…..there is so much wrong with FATCA and the war you are waging. you can not win…..you can only fiscaly damage america more and more……….

we need to have a massive across canada celibration in front of each united states consulate when the supreme court decision is announced in our favor.

Thank you Anne Frank for laying out so well what many of us know intuitively – that what the Canadian government is doing is just plain wrong. The Harper government is acting like snitches and ratting us out to get a better deal from the henchmen holding their master’s money ransom. That’s it.

I makes my blood boil to think I told told my MP, Conservative John Weston that my tax issues were between me and the US government and I had no reasonable expectation for the Canadian government to intervene on my behalf, then to have him and his government end up intervening to my detriment – and having the audacity to tell me that he’s “thrilled” about the great deal we wouldn’t have gotten otherwise.

Question: Because Canada has no law that allows for the imposition of taxes on it’s citizens wherever they live (CBT), is CBT in fact illegal in Canada, and therefore illegal for our government to endorse? Canada does not practice capital punishment and says NO when other nations seek to extradite their citizens when doing so would subject our citizens and permanent residents to execution. How is this situation any different?

And, when this is finally over, I can’t wait to start planning the “Gathering of the Brock” wherein we all get to come together to celebrate, meet each other, thank each other, congratulate each other, and marvel at the job we have done. It’s really incredible. Charter challenge by crowd sourcing! Donations of empathy, sympathy, understanding, expertise, experience, encouragement, AND money (of course). Onward!

Thanks so much, George. I have a conversation that may turn into an interview tomorrow. This helps.

And, there is a statement here that agrees: http://www.canadavisa.com/dual-citizenship-canada.html — The laws that apply to each individual depend on which country of citizenship the person resides in at that time.

**************

And, hypothetical only: A child being born in Canada to two US citizen parents (and the US defines is a US citizen from their first breath in Canada), which citizenship takes precedence? I say / continue to say, Canada — the country in which he (or she) takes that first breath — and all the others that follow in that country!!!!!!

@Calgary411, let me attempt to crudely citizenship in the same terms of faith/religion.

Can a person be a practicing Roman Catholic and a practicing Baptist at the same time?

Dual religion/faith does not and can not exist.

@ Anne Frank

Maybe that wonderful piece you wrote only froze at ADCSovereignty because it was too long. Could you split it into 2 or 3 parts and try again? Really, really good work — many, many thanks. And this is bang on: “Canada cannot help the US aim the gun, identify the victim and then deny any responsibility for the obvious and intended outcome.”

I particularly thank you for this part: “The arguments discussed above of course apply with still more force in the case of Canadian born US Persons who owe their unfortunate status to a Green Card not surrendered in the prescribed fashion for tax purposes or to having been born in Canada to US-born parents.”

I certainly agree. This discussion is not particularly for me.

No name,

What a lovely comment — and one many of us here have in mind at the end of this. In the meantime, we will continue donating all you say: empathy, sympathy, understanding, expertise, experience, encouragement AND that much-needed money to make the Canadian (and any other countries’) litigation a reality.

Onward, indeed!!!! http://www.adcs-adsc.ca/

Ok, maybe it’s a little desperate of me to suggest that what the Canadian government is doing is illegal considering we have a tax treaty with the US that allows for the execution of their tax laws in Canada, but couldn’t a strong argument be made that it’s unethical to enforce another nation’s laws that we don’t have in Canada? What do we stand for as a nation, if we can’t stand by our own laws as being just!

Yes, bubblebustin,

Ethics — the missing component of the Canadian Conservative government in their assertion that US law can / will / does over-ride Canadian laws and the Canadian Charter of Rights and Freedoms to make those the US defines as *US Persons* second-class to any other Canadians — no matter what their national origin or that of their parents / grandparents!

Nothing ethical about any of it. And, they all fall in line after Harper like dominoes.

JC has just pointed out that Anne Frank’s comment is now a major part of a new posting at ADCSovereighty:

https://adcsovereignty.wordpress.com/2014/11/19/how-the-fatca-iga-has-made-u-s-citizenship-a-disability-in-canada-and-highlighted-the-issue-of-law-firm-trust-accounts/#comments

And John says more to come.

Posted on ads.sovereignty.wordpress:

I read @Anne Frank’s comments and I think ‘game,set, match’ as long as it is all backed by legal action and goes through the courts.

One example left out: restriction on being Treasurer of neighborhood Girl Scouts.

In terms of “damages” above – it is implied damages the Canadian Government will bring onto its citizens as a result of C-31. “Damages” tends to be used in legal language that may also include redress, compensation, and class action lawsuit.

One may argue “damages” even for those not “outed.” Fear of consequences and the long arm of the IRS could influence people to make life altering changes and disadvantage them from a normal life. Then there is the stress inflicted by the Canadian and US governments.

Down the road it would be nice to have a class action lawsuit (with jury trial) for damages against the US on behalf of the nonUS family members impacted by the US laws. Within the family unit there is certain financial security inbuilt and recognized in law – such as there may be a breadwinner and one who has taken time off away from career to raise children. Say there is a breadwinner US person and they had their retirement savings and financial planning impaired by US tax law and they died relatively early and were subject to US estate law. Then this all would negatively impact on say nonUS citizen children and nonUS citizen spouse who would normally receive quite a bit more had not the US compliance and tax intervened.

@Anne Frank, please consider this angle of the sanctity of the family financial unit and impact of US laws on rights of family members.

@Anne Frank Excellent series of commentaries.

@NothernShrike re your comment; “…Nearest thing to the FATCA threat that I can come up with is international, in particular economic, sanctions….”

In terms of economic sanctions, see Prof. Arthur Cockfield’s work and comments on FATCA in which he mentions NAFTA;

ex. “…Under FATCA, the United States enacted a law that unilaterally imposes a tax or non-tax

measure that changes the nature of cross-border financial services provided by foreign

banks, including Canadian banks. These changes are clearly inconsistent with the spirit and

purpose of NAFTA. Moreover, the changes may violate specific provisions of NAFTA. As

mentioned earlier, the Implementation Act’s ‘inconsistency clause’ appears to try to

override NAFTA (and all other Canadian laws), which may or may not cure a potential

NAFTA violation….”

See particularly pages 43 to 46 of

SUBMISSION TO FINANCE DEPARTMENT ON IMPLEMENTATION OF

FATCA IN CANADA:

SUBMISSION ON LEGISLATIVE PROPOSALS

RELATING TO THE CANADA–UNITED STATES

ENHANCED TAX INFORMATION EXCHANGE AGREEMENT

Allison Christians*

Arthur Cockfield**

EXECUTIVE SUMMARY

http://alexatamanenko.ndp.ca/sites/default/files/multisite/2064/field_content_files/legal_paper_on_fatca_cockfield-.pdf

Prof. Cockfield also testified to that issue before Parliamentarians:”……..I believe it violates the NAFTA agreement. I’ve written a book on the topic of NAFTA tax law and policy, and it’s my opinion that FATCA, again, violates certain provisions within NAFTA.”

FINA-34 (May 13, 2014) http://parlvu.parl.gc.ca/Embed/en/i/8359630/?ml=en&vt=watch

http://www.parl.gc.ca/HousePublications/Publication.aspx?DocId=6597204&Language=E&Mode=1#Int-8359630

Prof. Cockfield received a grant from the Privacy Commissioner of Canada to study FATCA – and in part, the implications re NAFTA; “…the project will also examine the interplay of FATCA with other Canadian laws that protect taxpayer privacy such as the Income Tax Act, the Canada-United States Tax Convention Act and the North American Free Trade Agreement (NAFTA). …”

https://www.priv.gc.ca/resource/cp/2013-2014/cp_bg_e.asp

The resultant paper is open source, available free for download from SSRN

http://ssrn.com/abstract=2433198

So very interesting that the Canadian government will dispute the softwood lumber shingles and shakes issue under NAFTA for a period whose history is described; “…. The dispute dates back hundreds of years, but in the 1980s it turned nasty. The U.S. has slapped billions of dollars of fines on Canadian wood, jeopardizing thousands of jobs. The dispute raises serious questions about trade, sovereignty, and the real nature of Canada-U.S. relations.” http://www.cbc.ca/archives/categories/economy-business/trade-agreements/at-loggerheads-the-canada-us-softwood-lumber-dispute/canada-wins-nafta-appeal.html , but not dispute the trade issues/economic sanctions issue of FATCA.

I commented on this here because the softwood lumber issue was recently in the news again http://business.financialpost.com/2014/10/31/the-granddaddy-of-all-canadian-u-s-trade-disputes-is-about-to-rear-its-ugly-head-again/http://isaacbrocksociety.ca/2014/02/09/the-myth-of-reciprocity/comment-page-2/#comment-2684862

Don Whitely raised this issue in his article ‘Canada Capitulates on FATCA Agreement’

Feb 7, 2014 “For the U.S., it’s arguably the most successful assault on Canada since the War of 1812. A close rival for that claim might be the 2006 softwood lumber capitulation (also orchestrated by the Harper government), but this tax-sharing agreement negatively affects far more Canadians and for much longer….”

http://www.bcbusiness.ca/finance/canada-capitulates-on-fatca-agreement

FATCA was meant to disadvantage and burden all the world’s financial (and many non-financial institutions) except those in the US – and have the rest of the world pay for its implementation and ongoing maintenance- forever and ever…. See; “….FATCA’s enforcement mechanism is both potent and innovative….” say Blank, Joshua D. and Mason, Ruth “Exporting FATCA” http://ssrn.com/abstract=2389500

FATCA was never contemplated as something reciprocal – or something to burden US banks with, which gives US banks a substantial advantage and lower operating costs, that and CBT and FBAR act to deny Canadians access to the same bank experience as their fellow Canadian citizens – and their fellow US citizens resident in the US.

I can’t see how that is not a trade issue, and how the threat of the 30% withholding is not a clear unwarranted economic sanction.

@Anne Frank, thank you for all your comments – of much assistance to layperson readers.

@Badger – @Neil points out proof that FATCA was never meant to be reciprocal: while the nations of the world were negotiating and requesting and saying they won victories on the exemption of reporting on pension and retirement accounts, supposedly because this would be too difficult or highly unlikely vehicles of tax evasion – the US did not request the same exemption. Why bother if you were not really interested in pursuing reciprocity.

The fight against FATCA is on in France :

http://www.frederic-lefebvre.org/fatca/

@EmBee et al

“And it came to pass in those days, that there went out a decree from Obamaugustus, that all the world should be taxed.” …

Yes, and with his new immigration announcement he will be putting millions more on the tax roll