UPDATE January 24, 2015: THIRD OF FIVE LEGAL BILLS PAID

[We now have a NEW POST taking us up to May 1, 2015. This post will be retired from service.]

On August 11, 2014, Constitutional Litigator Joseph Arvay filed a FATCA IGA lawsuit in Canada Federal Court on behalf of Plaintiffs Ginny and Gwen, the Alliance for the Defence of Canadian Sovereignty (en français), and all peoples worldwide. Read Alliance’s Claims and comment on our Alliance blog.

Chers amis et donateurs,

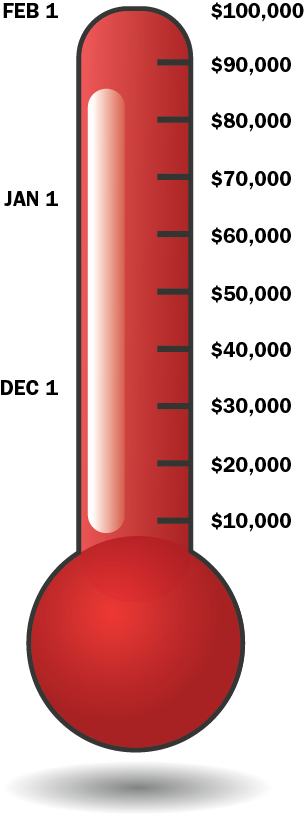

Ensemble, nous avons atteint notre but : ramasser les fonds nécessaires pour payer la troisième des cinq factures légales de notre poursuite judiciaire.

Ramasser 300 000 $ provenant de petits dons est un exploit tout à fait extraordinaire et nous invitons notre gouvernement canadien, ainsi que tous les autres gouvernements qui ont piétiné les droits de leurs citoyens, à en prendre bonne note.

Chaque jour, nous nous rapprochons de notre but. Déjà, nous avons ramassé plus de la moitié des fonds nécessaires pour payer les frais légaux de notre poursuite contre le gouvernement canadien et l’entente FATCA.

Si nous avons parcouru un si grand bout de chemin, c’est grâce à nos deux courageuses plaignantes, Ginny et Gwen, à nos donateurs provenant du Canada et de partout dans le monde, ainsi qu’aux administrateurs des sites Internet Isaac Brock Society et Maple Sandbox. Ils permettent tous à nos voix d’être entendues.

Merci !

L’équipe de l’ADSC

———————————————————————————————–

Dear Friends and Supporters,

Together we have reached our goal of paying off the third of five retainer fees for our Canadian FATCA IGA lawsuit.

Raising $300,000 from small donations is a pretty amazing achievement and we ask the Government of Canada, and those other governments who have also tossed away rights of their citizens, to take notice.

It’s still a marathon, but we are more than half way to pay off the Federal Court legal costs.

We have come so far because of our brave Plaintiffs, Ginny and Gwen, our Canadian and International donor-supporters, and the administrators of the Isaac Brock and Maple Sandbox websites who make it possible for our voices to be heard.

Thank you all,

—The ADCS-ADSC team

Also to show discrimination the Governments needs to answer the following questions –

If you had 100 Canadian citizens with a US place of birth what percentage would be reported to the IRS?

If you had 100 Canadian citizens with a Canadian place of birth what percentage would be reported to the IRS?

Now of course is 100% for the top and the Canadian Government could argue people in the bottom question has made themselves a ‘US Person’ in some fashion, but even then the percentage would be small.

But the difference is the Government really could make an argue against the 100% and equally couldn’t argue 100% in second question would ever get reported.

So in my mind it’s discrimination – but of course they’d just lie and write lots of courtroom fiction hoping a jury or judge will believe it.

This particular assertion, from paragraph 46 of the gov’t’s response, is particularly scary IMHO:

“Furthermore, the defendants deny that there exists a principle of fundamental justice that foreign tax debts are not enforceable in Canada. “

@Dash,

The government has already lost several important cases. I can imagine (and would certainly hope), that something (as you have quoted) that so grossly violates The Revenue Rule, which IS law in Canada, will be seen by the courts as indefensible.

I have the distinct impression this response was not written by a constitutional expert.

Do they have any in the Department of Justice? Perhaps that explains their dismal record before the Supreme Court.

@ Tricia What is The Revenue Rule? Does this have something to do with Canada helping a foreign government collect taxes and penalties from Canadian citizens resident in Canada? The former Finance Minister, Jim Flaherty, was quoted as saying this in a news article. I have heard this is in a treaty but is this actually a law?

@Blaze

And here are 5 reminders:

@anniegirl1138 Here are 5 cases Harper govt has already lost http://bit.ly/1xFhO2H At least 1 other b4 courts now -Bill C-24 /citizenship

And one more in progress:

@anniegirl1138 Galati takes on Bill C-24 http://on.thestar.com/10Opd4t

@heartsick,

Yes it is and it is law in the US as well. Allison Christians has spoken of this often. I’ll find something and post soon………. rooted in common law…………..

@blaze

I think Gerald Keddy’s found a new job.

Good one, bubblebustin!

@ Bubblebustin Thanks for the laugh. I haven’t read the whole reponse but from the comments it does seem that he might have a hand in it. Clueless, that’s all I can say. So sad that our government no longer feels its job is to represent us, the people. Time to send in another donation.

@bubblebustin

OMG that’s funny!

Perhaps we could just submit some “amendments” on his behalf….you know…”You’re either an American citizen or……….make it easy for them ;-P

@heartsick

These are excerpts taken from Prof Christians’ testimony before the Standing Committee on Finance on May 13, 2014. They are somewhat out of context in that I am not including some of the questions that preceded her answers after the initial statement in order to avoid recreating the entire proceeding. What is interesting is to note how strongly she emphasizes it and how thoroughly the committee ignored it’s relevance. Any emphasis is mine.

end of opening statement regarding the revenue rule

*****

*****

******

***

written transcript available at:

http://www.parl.gc.ca/HousePublications/Publication.aspx?DocId=6597204&Language=E&Mode=1

video:

https://www.youtube.com/watch?v=YxJf_Lk-yig

Allison’s opening remarks open the session.

Unfortunately, other academics have differing views about The Revenue Rule…….

Demise of the revenue rule in tax law

By Vern Krishna

The Lawyers Weekly, Vol. 24, No. 24 (October 29, 2004)

“The traditional rule that a country will not enforce the revenue laws of another country and that no

country is under an obligation to disclose financial information to foreign governments is very

much on its way to extinction.”

Professor Vern Krishna, CM, QC, FCGA, is Counsel, Borden Ladner Gervais LLP, and executive

director of the CGA Tax Research Centre at the University of Ottawa.

http://www.google.ca/url?sa=t&rct=j&q=&esrc=s&source=web&cd=4&ved=0CDUQFjAD&url=http%3A%2F%2Fwww.commonlaw.uottawa.ca%2Findex.php%3Foption%3Dcom_docman%26task%3Ddoc_download%26gid%3D1504&ei=2b9hVLCJOYi2oQTd3IL4Bg&usg=AFQjCNHRGpRJUXRcSn_vhPAoF0hCuyyTVA

@Shovel

@Tricia Moon

I don’t think Professor Krishna’s 2004 paper is in conflict with Professor Christians remarks if you read them both carefully. Professor Krishna’s paper draws that conclusion as an OPINION based almost exclusively on the example of the Cayman Islands’ situation. There is no reference to the Canada/US relationship in the analysis or conclusion. That paper is 10 years old.

Professor Christians, on the other hand, is specifically using the Canada/US relationship and existing laws of those countries (including the Revenue Rule). She refers to the FACT that the Revenue Rule does indeed exist in both countries, including the US.

“39. ….. Nothing in the Impugned Provisions results in different treatment of U.S. citizens resident in Canada than Canadian citizens resident in Canada who may themselves be liable to pay U.S. taxes.” OH YES IT DOES!! A Canadian citizen, resident in Canada who otherwise would have no “obligation” to pay (file) U.S. taxes, immediately is seen to have such obligation when a U.S. birthplace is revealed. No other birthplace (except Eritrea) is accompanied by such a curse. Therefore, this statement of response by the Attorney General is completely in error.

“45. ….. if the Impugned Provisions expose the plaintiffs to any deprivation of liberty or security of the person, which is denied, such deprivation occurs in accordance with the principles of fundamental justice.” MY GAWD! The Attorney General is telling Ginny and Gwen and all of us that we DESERVE what is happening to us. This response is simply appalling.

“48. ….. The plaintiffs, and other U.S. persons, have pre-existing obligations to provide account information themselves to U.S. taxing authorities ….. ” NOT IF WE ARE CANADIANS LIVING IN CANADA, even if we are, in some way, also considered US Persons. According to the 1930 Hague Convention (still in effect) which dealt with the issue of multiple citizenships, when a person is living in the country of one of his citizenships, the country of his other citizenship has no hold on or jurisdiction over that person.

I have submitted this idea to Mr. Arvay’s team already through another thread some time ago. I will post a reminder of it on the ADCS site as suggested in today’s headline.

I see that the ADCS blog is a Facebook blog and I don’t do Facebook so I will post the details of my above comment here. I sincerely hope Mr. Arvay and his team will look into this aspect of our case. This is a quote from one of my many communications with the Canadian government.

“To deal with the increased prevalence of the instance of dual citizenship in the last century international norms were established. Ironically, my first quote is from the U.S. Department of State Foreign Affairs Manual Volume 7: Consular Affairs:

“’It is a generally recognized rule, often regarded as a rule of international law, that when a person who is a dual national is residing in either of the countries of nationality, the person owes paramount allegiance to that country, and that country has the right to assert its claim without interference from the other country.’ (emphasis mine)

“The ‘rule’ referred to above is an expansion on Article 4 of the 1930 Hague Convention on Certain Questions relating to the Conflict of Nationality Laws which is still in effect. My second quote is an interpretation of this same Article by the Home Office of the United Kingdom:

“’…the practical effect of this Article is that where a person is a national of, for example, two States (A and B) and is in the territory of State A, then State B has no right to claim that person as its national or to intervene on that person’s behalf.” (emphasis mine) http://www.bia.homeoffice.gov.uk/sitecontent/documents/policyandlaw/nationalityinstructions/nisec2gensec/dualnationality?view=Binary

“There is nothing in either of these sensible statements to suggest that the matter of taxation is to be considered an exception. In short, in Canada the dual Canadian/American citizen is a Canadian, and a Canadian only. The FATCA IGA contravenes this long-standing international practice by placing greater importance on the Canadian-resident dual citizen’s relationship to the United States than on his relationship to Canada, the country of his dominant nationality.”

Doing away with the revenue rule would work well in a world that would like to do away with financial privacy altogether. Privacy is a hot topic right now, and people are pretty divided about it. In one camp there are those out there who’d give away all of our personal and financial privacy to catch a few terrorists and tax evaders. Then there are those who know the difference between privacy and secrecy and appreciate what privacy brings us in terms of liberty.

The best we can hope for is a conservative judge (small c) from an ethnic group sensitive to persecution.

@MuzzledNoMore

The ADCS WordPress blog is here:

http://adcsovereignty.wordpress.com/2014/11/10/the-government-of-canadas-statement-of-defence-to-adcss-statement-of-claim/#comments

The government’s response tells us that they’re “stuck on stupid”.

@Muzzled,

The Alliance blog that I provided a link to (at the top of this thread) is NOT a facebook blog.

You can re-post your suggestions on this link: https://adcsovereignty.wordpress.com/2014/11/10/the-government-of-canadas-statement-of-defence-to-adcss-statement-of-claim/

This is a post meant specifically for “Statement of Defence” related thoughts and suggestions.

I don’t do facebook either.

I have reviewed the Statement of Defence and would generally comment that they have not exactly stretched themselves. It is fairly pro forma, but there are some interesting glimpses into the strategy that will be deployed. All should please note that the Defence is primarily to plead FACTS not make arguments of law. As a Charter challenge based on a law, this case will be primarily fought on the field of legal arguments with facts – including hypothetical facts – providing only a very loose framework for the debate. In short, the Defence appears sparse because it is and it is because they have chosen to keep much of their legal strategy to themselves for the time being. There is good and bad in that – the good of course is that, there being few facts to debate, the obstacles to getting an early hearing date will be that much fewer.

This being said, I thought I’d provide a few comments:

para 8: Inclined to comment “why bother?”. They plead that the tax treaty addresses the elimination of double taxation. Perhaps the more accurate statement is that the tax treaty purports to set the goal of the elimination of double taxation and then, by permitting the maintenance of CBT exceptions (US insistence on this is one reason it has so few treaties), effectively contradicts itself and fails. The treaty reduces some aspects of double taxation is the best that can be said of it. Further, the USG has retained the right to override the treaty by subsequent measures which it has chosen to exercise on numerous occasions.

para 11: this is really a pretty important concession. It notes that FATCA is aimed both at actual and POTENTIAL US taxpayers. This concession is repeated in a number of other places in the Defence. The importance of it is this: it may be one thing to say that Canada, as a matter of (bad) public policy is going to help the US assess (but not collect? – more on this later) taxes that are due under its own law upon Canadian citizens or residents. It is another thing entirely to say that Canada will round up hundreds of thousands of likely suspects, violate their privacy rights and allow the IRS to sift through their data to see which ones might warrant greater interest. By definition, the net hauls in the “guilty” and the innocent. Violating the Charter rights of these latter innocent parties to help find the guilty for a foreign power takes the Charter analysis to a whole other level. Of course we would challenge the premise of “guilty” head on as well, but my point is the Defence concedes from the outset that FATCA (and by extension C-31 which enforces it in Canada) will turn up data relating to NON-US taxpayers and forward same to the US. That is a really, really huge point and one which sets the Charter barrier all the higher for the Defence to justify under s. 1. By way of aside here, I would gently criticise the Statement of Claim to a minor degree on this point. Para. 24 of the Claim implies that a CLN is the ONLY way in which US double tax liability can be extinguished via relinquishment. That is true today under the Tax Code, I agree. However, prior to the 90’s, there was no obligation to seek a CLN in order to have relinquishment recognized for tax purposes. Anyone with a “grandfathered” act of relinquishment is also not a US taxpayer but would have indicia that would cause FATCA to sweep them up and turn them over. Thus two categories of by-catch have data that C-31 turns over to the IRS in violation of their privacy rights: spouses, business partners and other parties having some financial connection to a “US Person” without necessarily knowing the tainted ethnic or national status of their partner; and (ii) former US Persons who relinquished by do not have and neither have nor ever had an obligation to obtain, a CLN.

Also note – and this is not unimportant – FATCA turns people over to the Treasury FBAR/FINCEN police (who happen to be the IRS as well). The FBAR regulations have little to do with tax. Their original justification in the 70’s was to monitor foreign exchange transactions that were allegedly undermining the US dollar (as if it hadn’t been undermined by Nixon abandoning Breton Woods and the convertibility of foreign central bank dollar reserves into gold). The in terrorem fine and penalty threats come primarily from this completely abused and misused statute primarily although obviously the Tax Code has its share of nasty compliance tools as well.

para 15-16: pretty much admits that extortion and threats are the reason for C-31. The corollary of this is that Canada chose to sacrifice the Charter rights of the few to preserve the trading and commercial privileges of the many. That will be an interesting debate under s. 1! One is always slow to make parallels to the Nazis, but it is hard to avoid sometimes. Was Vichy justified in filling trains with French Jews to avoid further sanctions from the Nazis? If not in those circumstances, where exactly does one draw the line? The whole point of the Charter, after all, is to protect minority rights from being sacrificed to the convenience or whim of the majority. Section 1 invites a weighing of the rights of the minority against the legitimate desires of the majority to be sure, but will FATCA come out a winner when the only Canadian interest at stake is the right of Canadian banks to carry on business in the US without interference (especially when they arguably already have that right – and tools to defend it – under NAFTA)? Bear in mind that work-arounds, while perhaps adding transaction costs, are eminently feasible. The Bank of Canada, for example, could be the clearing house for US dollar transactions. Canada US trade could be denominated in C$ instead of US$ or indeed even in Euros for that matter. Commerce would find a way around FATCA, there is simply no doubt whatsoever. It is doing so right now in the countries that are too poor to be able to afford an IGA with the US. Canada didn’t stand up to the US, so we’ll never know whether the FATCA bluff could have been called by the largest trading partner of the US. In short, the s. 1 weighing exercise can’t simply assume 30% tax = commercial armageddon for Canada. Rather, it means significant adjustment cost, bother and uncertainty, but whether this “cost” was greater or lesser than the billions of costs FATCA is imposing with Canada’s blessing is another matter (and note, those expenses are tax deductible IN CANADA and thus costing OUR government real money). THIS is what was avoided by caving in and tossing the minority to the wolves. This is the true s. 1 debate that Mr. Arvay will join.

para. 18 – discussion of tax treaties implies that C-31 and FATCA is right in line with these. In fact, it is hugely different in kind. The tax treaties allow a case-by-case automatic exchange of information about named individuals and are conditioned by safeguards including such things as reciprocity and specificity. I will only give you information for a particular taxpayer if you request it by name and with enough particularity to establish your right to it. It is the difference between a search warrant directed at John Doe living at 123 Main Street and a warrant to search every house in town to see what you can find. There’s bound to be a tax cheat somewhere in town, let’s search every house until we find one.

para. 20-22: If Justice is going to plead reciprocity from the US as justifying C-31, they have just left themselves open to a finding that lack of reciprocity is a virtual certainty. The US eschewing GATCA ought to leave little doubt. OECD’s GATCA, of course, is premised on RBT not CBT and the US wants only what it wants, not what anyone else wants. The US is in fact the repository of billions if not trillions of “safe haven” funds being hidden from governments of countries all over South America, Africa, Asia etc.The US banking policy is “don’t ask and certainly don’t tell” and FATCA has not changed that. The US has more foreign deposits than Canada does to be sure and is in no hurry to lose them.

para 32 – the premise of this one is amusing. The Agreement “eases the burden” of FATCA. Actually, C-31 CREATES the burden. What they are doing is crowing that the burden could have been harsher if Canada had agreed to harsher burdens. Be happy I’m only chopping off your hand – I could have chopped off your arm if I wanted to! The whole statement is absurd and irrelevant. FATCA is US law and has no application in Canada. It NEVER could have been applied in Canada by any FI since application of it in Canada by a Canadian FI would have violated Canadian law. That was the status quo until C-31 changed it. Behaviour which was formerly illegal – refusing to deal with Canadians or turning over private Canadian financial data to a foreign government – became LEGAL under C-31. The fact that C-31 could have been still harsher does not add much to the analysis of whether C-31 passes Charter muster. The fact that Canada got the standard form template IGA with no greater benefits that were received by any other country (large or small) that signed one is also a pretty obvious rejoinder here. The IGA contemplated listing exempt account types like RRSP’s. Canada didn’t bargain for it – they got to list their exempt accounts on the form the same way everyone else did. The accounts will still get confiscated by the IRS – just one step later (after reporting of the other accounts to the IRS by the CRA causes the hapless “US Person” to be threatened with jail and personal ruin for the crime of having lived outside the US in compliance with local laws).

para 32(f) is a personal laugh riot. Pleading that Canadian law is somehow paramount here is opening them up to ridicule. The Agreement is stated to be paramount and the Agreement incorporates US law, including US law as it changes from time to time, in more places than I can take the time to count. The US has changed its citizenship law on a number of occasions as many here have pointed out. Canadians have been variously “in” and “out” of the US dragnet at the whim of these changes over time. Green card holders who return to Canada in ignorance of the IRS’s precise code for abandoning their Green Card for tax purposes – a not inconsiderable number as well – are a chapter unto themselves. Under the US tax code, they have perpetual tax obligations without even the theoretical possibility of residence in the US.

para. 37 – the question has to be asked: if the Exchange of Information is NOT in aid of collection of taxes, what on earth is the point? What is enforcement of tax law if not collection? Tax law does not seek information for information’s sake. It seeks information for money’s sake. Why is Canada sending private data to the IRS which the IRS certainly tells Congress is useful for collection purposes – to the point of including incremental revenues estimated to be raised from it in the US budget – while telling the Canadian court that it is just about exchanging information not money? This is not two scientists sharing data that will help grow the common wealth of scientific knowledge of mankind after all. This is private financial information which has only one use: to threaten the owners of that data within things they don’t want to be threatened with. Not a convincing argument.

para 38 – note again, persons who are or “potentially” are subject to US tax. It may be relevant to US tax, but then again, it may not. Besides, tax of course is on INCOME and we all know that having a bank account with money in it is pretty much the LAST PLACE ON EARTH you can look to for income in any event! On a more serious note, having assets is not the same as having tax liability. Tax liability is actually based on income – I wasn’t joking when I said that – and account information is a tool to audit, not to claim. In short, it is a fishing expedition even when aimed at a particular person as opposed to a class of them. Homelanders don’t report assets, Canadians don’t report assets. They do report interest income over a threshold. FATCA is a quantum leap in intrusiveness and breach of privacy in search of tax that MIGHT be owing, not that IS owing. If, as the Defence notes, the tax treaty already eliminates double taxation of Canadian residents, what possible purpose is served by further exchange of information?.

para. 39 – keep your blood pressure in check. Keddy wrote this one (contrasting “US citizens resident in Canada” with “Canadian citizens”. If you feel like a “mudblood” reading that, raise your hand)! Once again, all “Canadian citizens” who “may” be liable to pay US taxes are caught. True enough. They are caught if they have enough US ancestry to be caught (Charter anyone?), as well as if they have had the misfortune to marry or go into business with one. Note again the “may” be subject to US tax argument. Anyone who “may” be subject to US tax also, by definition, may not. Unstated in all of this is that the persons who “may” be subject are thrown to the US wolves and forced to defend themselves in US courts under US law to establish that they were never subject to US law in the first place. Catch 22. Might one expect the Charter to allow Canadians to have their rights and obligations arising out of their income and activities IN CANADA be subject to Canadian courts and Canadian law?

para 49, 52 and 53 – this is a doozy. Makes very clear that the violation of the Charter rights are only as much as was needed to protect the commercial interests of banks carrying on business outside of Canada. Wow. That is stark, but at least puts the debate on the proper plane.

(nb- this whole section of the Defence is what I referenced above: pretty much a blanket denial saving the legal arguments for later)

By and large, the real arguments are not going to come out until they file their written arguments just before the hearing. This is interesting is how LITTLE it does say. They really show no signs of intending to elicit much by way of evidence.

@Anne Frank

RE: “para 15-16: pretty much admits that extortion and threats are the reason for C-31. The corollary of this is that Canada chose to sacrifice the Charter rights of the few to preserve the trading and commercial privileges of the many.”

NB:

There is legal precedent in Canada that the effects of foreign laws are a BUSINESS RISK that Canadian banks take on voluntarily.

In Van deMark vs. Toronto Dominion Bank [1989], a Canadian court decision established two important principles:

– in a conflict of laws, Canadian law has primacy over the law of a foreign jurisdiction where the bank also does business; and

– Canadian banks may not act as foreign revenue collectors or enforcers.

That judgement stated:

“There is no dispute between the bank and Kenneth Van deMark and the dispute, if any, is between the bank and the Internal Revenue Service of the United States. The effect of what has occurred is that a Canadian citizen has placed assets in a branch in Canada of a Canadian chartered bank. The bank also does business in the United States and is being threatened by a United States authority.”

“One must sympathize with the position of the bank but that position is the result of its election to carry on business in more than one country and that cannot influence the application of Canadian law.”

“In any event, while acceptance by the bank of a penalty imposed in the United States might seem to be a hardship, the effect of permitting the Ontario branches to defend the applicants’ claim on the basis of the bank’s liability in New York State would be to enforce indirectly a claim for taxes by a foreign state… and one that has, so far as the evidence discloses, not even given rise to a New York or Federal Court judgment.”

@Anne,

Thanks. I have forwarded your analysis to the members of the Arvay team.

@AF

Now what could the defence possibly have up their sleeve? Of course by discussing, we may just give them ideas they haven’t thought of themselves.